Question: Question 22 Given the following infromation, use the biniomial option pricing model to determine the price of this European call option. Round your final answer

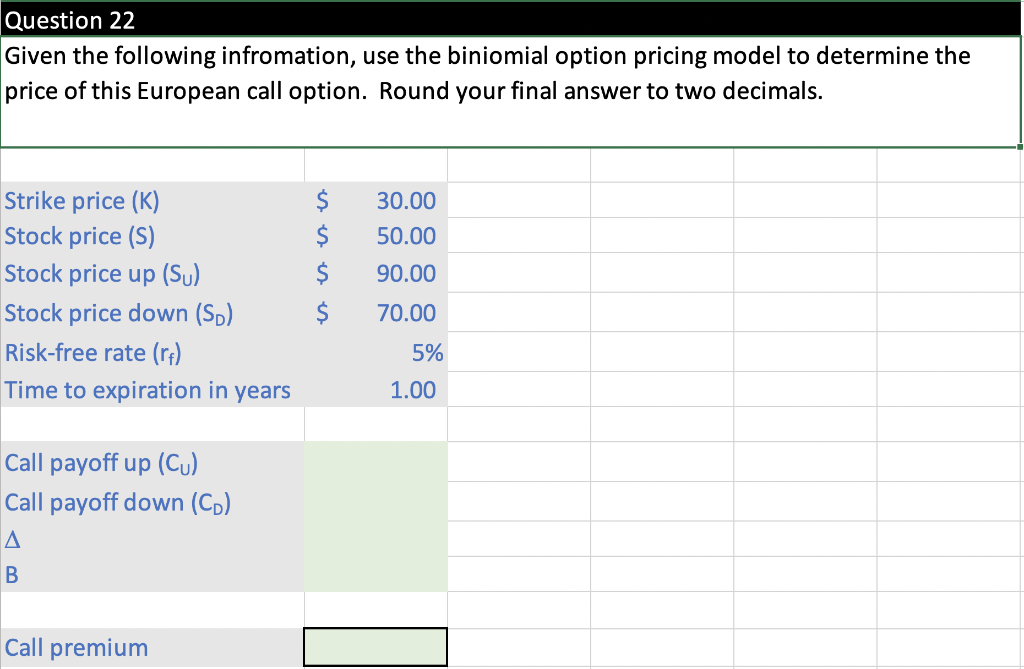

Question 22 Given the following infromation, use the biniomial option pricing model to determine the price of this European call option. Round your final answer to two decimals. Strike price (K) Stock price (s) Stock price up (su) Stock price down (Sp) Risk-free rate (rf) Time to expiration in years $ $ $ $ 30.00 50.00 90.00 70.00 5% 1.00 Call payoff up (Cu) Call payoff down (CD) A B Call premium

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock