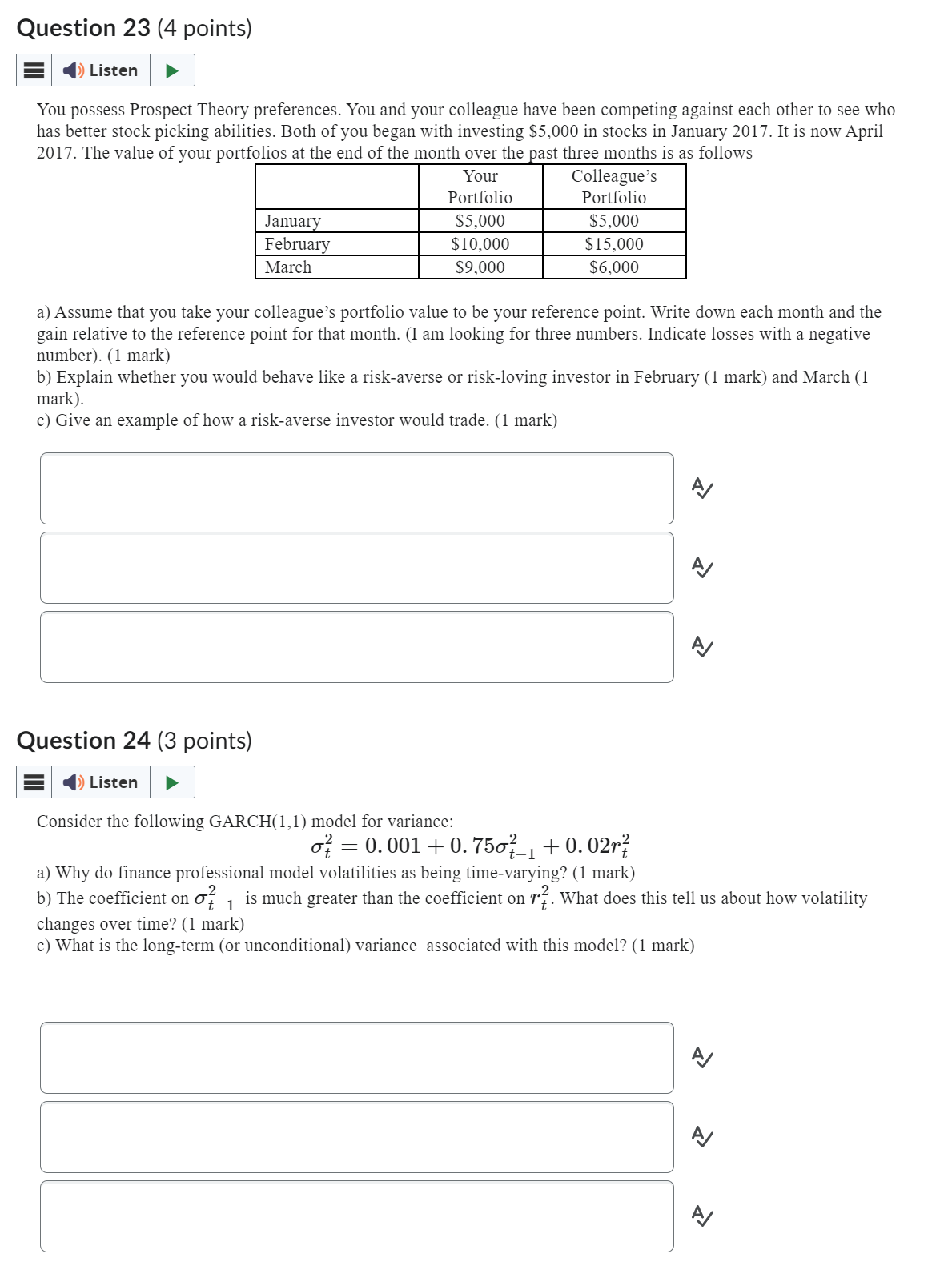

Question: Question 23 (4 points) E (ijListe-n b l You possess Prospect Theory preferences. You and your colleague have been competing against each other to see

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts