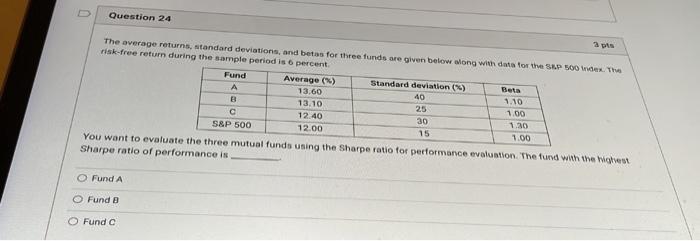

Question: Question 24 OS The average returns, standard deviations, and bets for three funds are given below along with data for the SAP NOW. Thus risk-free

Question 24 OS The average returns, standard deviations, and bets for three funds are given below along with data for the SAP NOW. Thus risk-free return during the sample period is 6 percent Fund Average (4) Standard deviation (") Beta 13.60 40 1.10 B 13.10 25 1.00 12.40 30 1.20 S&P 500 12.00 15 1.00 You want to evaluate the three mutual funds using the Sharpe ratio for performance evaluation. The fund with the waves Sharpe ratio of performance is O Fund A O Fund a O Fundo

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock