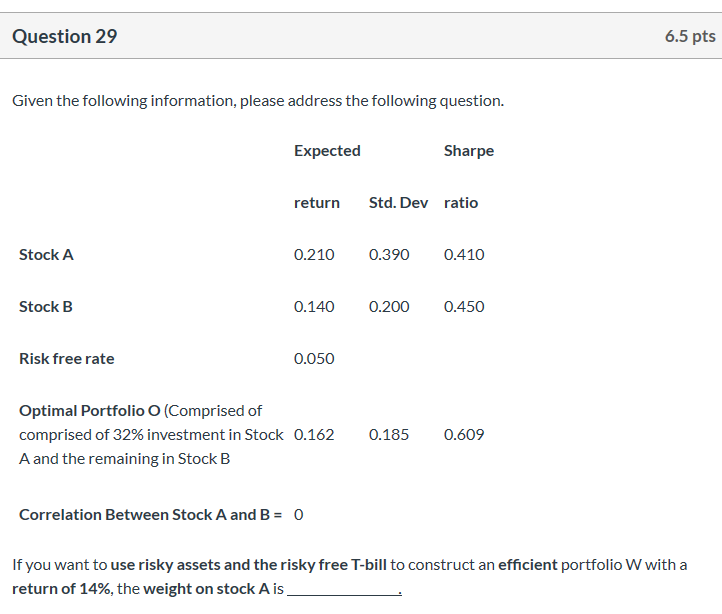

Question: Question 29 6.5 pts Given the following information, please address the following question. Expected Sharpe return Std. Dev ratio Stock A 0.210 0.390 0.410 Stock

Question 29 6.5 pts Given the following information, please address the following question. Expected Sharpe return Std. Dev ratio Stock A 0.210 0.390 0.410 Stock B 0.140 0.200 0.450 Risk free rate 0.050 Optimal Portfolio O Comprised of comprised of 32% investment in Stock 0.162 A and the remaining in Stock B 0.185 0.609 Correlation Between Stock A and B = 0 If you want to use risky assets and the risky free T-bill to construct an efficient portfolio W with a return of 14%, the weight on stock A is

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock