Question: QUESTION 2ANSWER ALL PARTS Explain how default occurs for a limited liability company within a structural model. How does the Merton model predict probability of

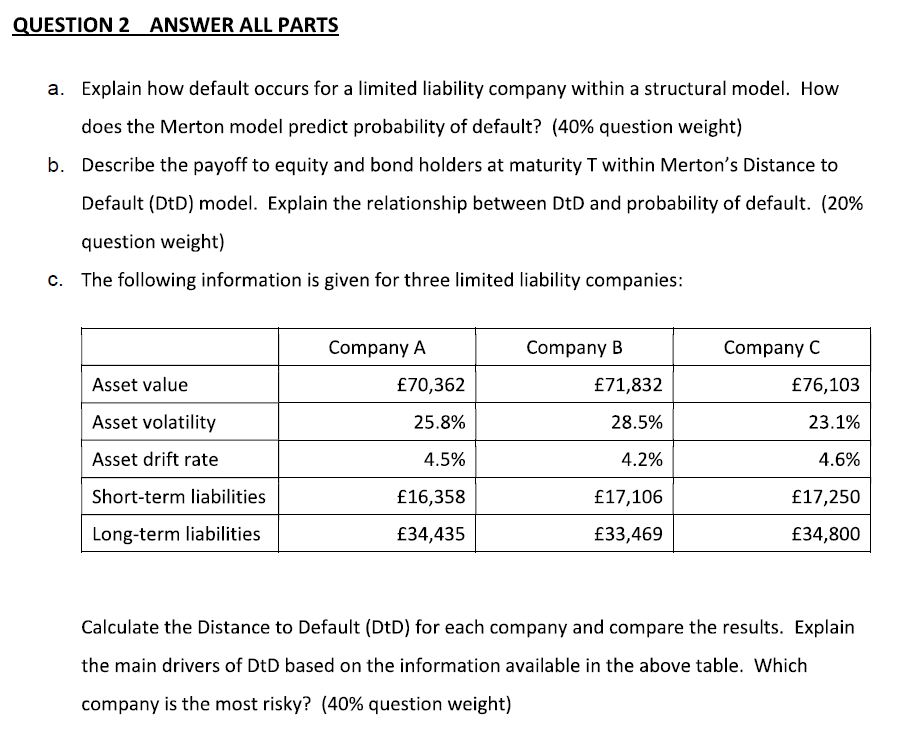

QUESTION 2ANSWER ALL PARTS Explain how default occurs for a limited liability company within a structural model. How does the Merton model predict probability of default? (40% question weight) Describe the payoff to equity and bond holders at maturity T within Merton's Distance to Default (DtD) model. Explain the relationship between DtD and probability of default. (20% question weight) The following information is given for three limited liability companies: a. b. c. Company A CompanyB Company C Asset value Asset volatility Asset drift rate Short-term liabilities Long-term liabilities 70,362 25.8% 4.5% 16,358 34,435 71,832 28.5% 4.2% 17,106 33,469 76,103 23.1% 4.6% 17,250 34,800 Calculate the Distance to Default (DtD) for each company and compare the results. Explain the main drivers of DtD based on the information available in the above table. Which company is the most risky? (40% question weight)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts