Question: Question 3 0 / 5 pts Julie Wells has found a Treasury Bond futures contract that has a duration of 8.5 years and is currently

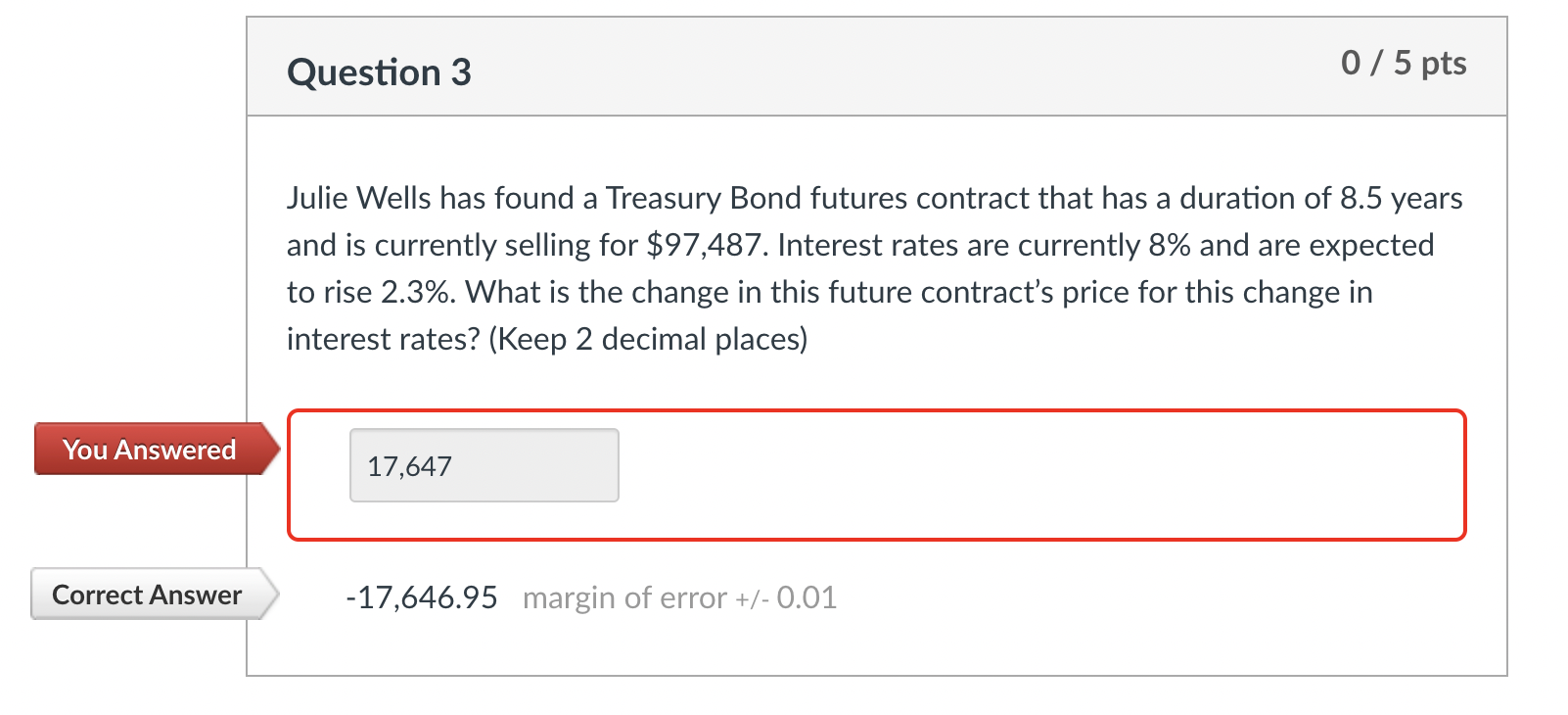

Question 3 0 / 5 pts Julie Wells has found a Treasury Bond futures contract that has a duration of 8.5 years and is currently selling for $97,487. Interest rates are currently 8% and are expected to rise 2.3%. What is the change in this future contract's price for this change in interest rates? (Keep 2 decimal places) You Answered 17,647 Correct Answer -17,646.95 margin of error +/- 0.01

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock