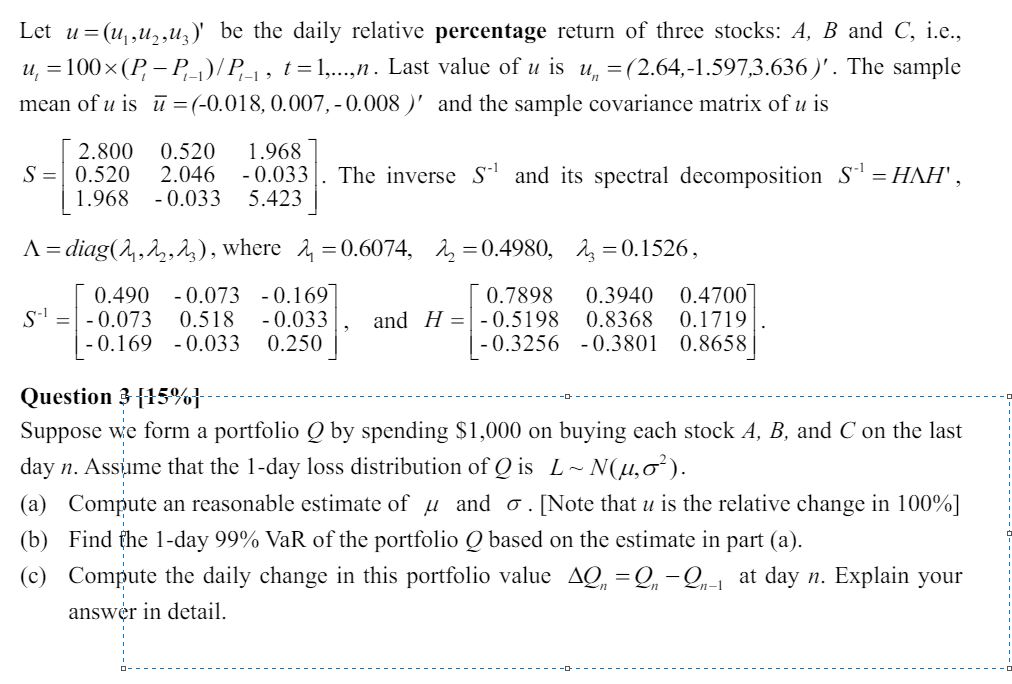

Question: Question 3 [ 1 5 % } - Suppose we form a portfolio Q by spending $ 1 , 0 0 0 on buying each

Question

Suppose we form a portfolio by spending $ on buying each stock and on the last

day Assume that the day loss distribution of is

a Compute an reasonable estimate of and Note that is the relative change in

b Find the day VaR of the portfolio based on the estimate in part a

c Compute the daily change in this portfolio value at day Explain your

answr in detail.

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock