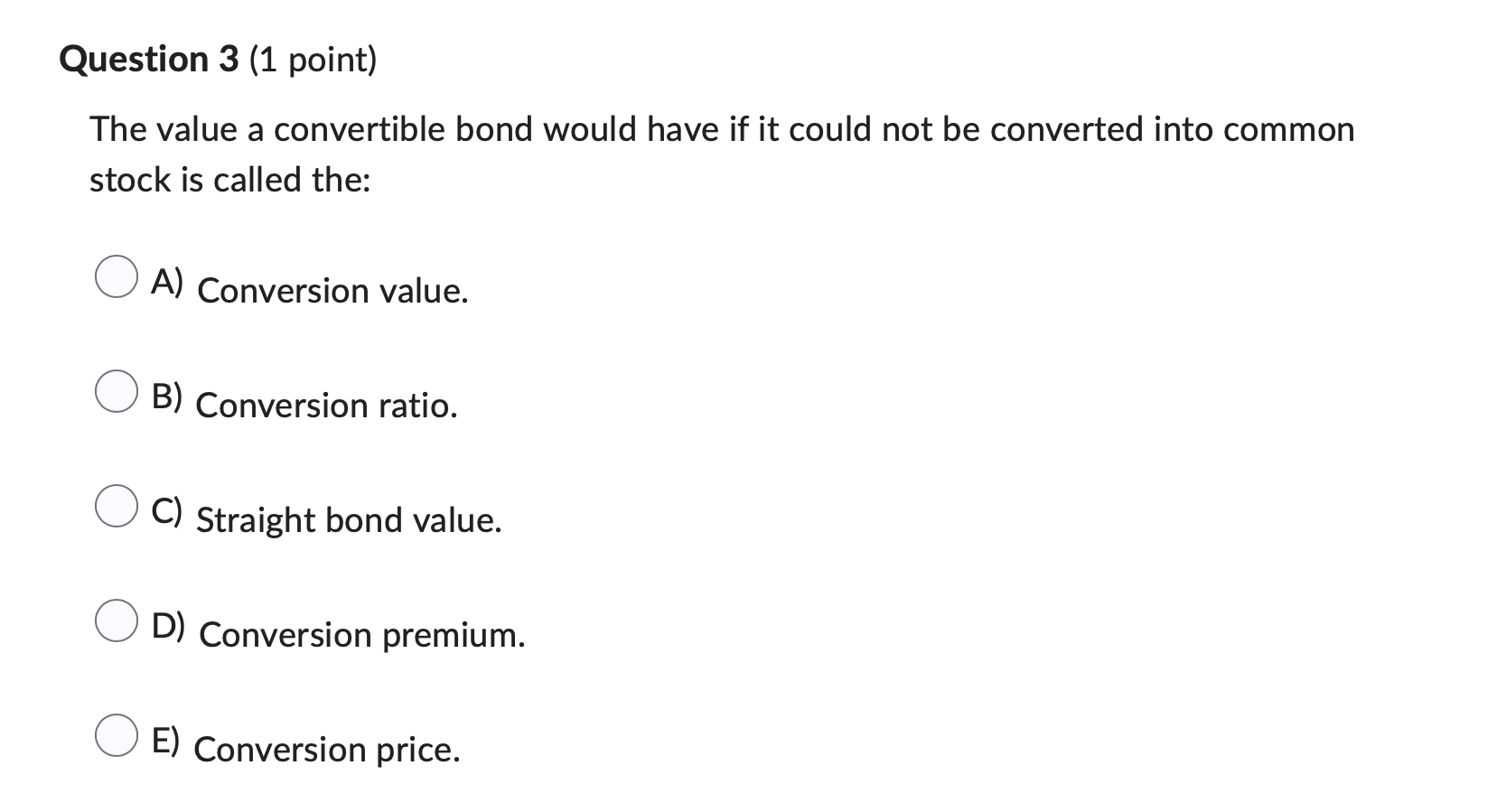

Question: Question 3 (1 point) The value a convertible bond would have if it could not be converted into common stock is called the: O A)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts