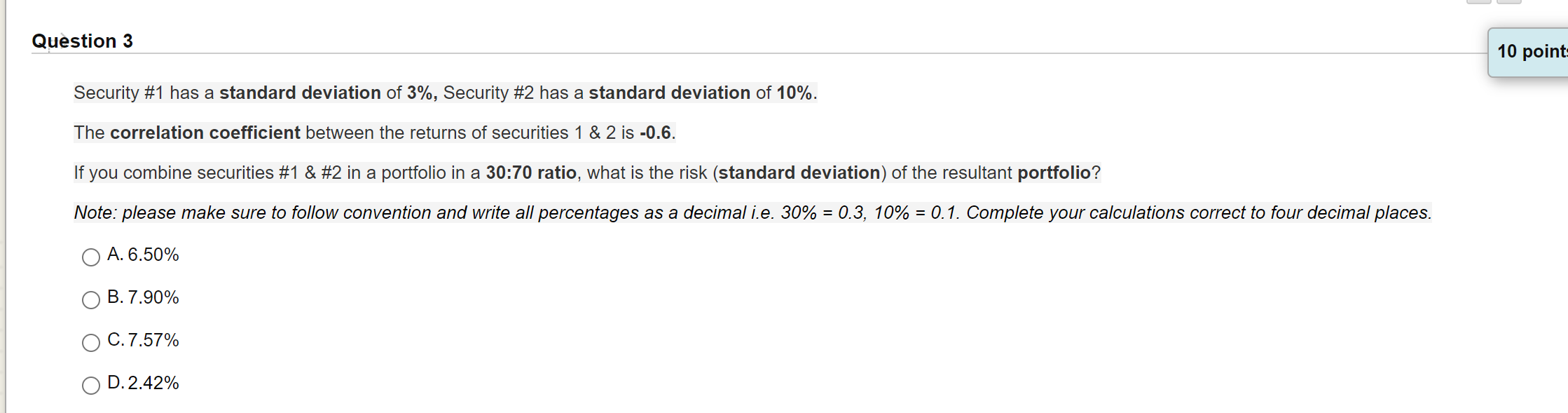

Question: Question 3 10 point Security #1 has a standard deviation of 3%, Security #2 has a standard deviation of 10%. The correlation coefficient between the

Question 3 10 point Security #1 has a standard deviation of 3%, Security #2 has a standard deviation of 10%. The correlation coefficient between the returns of securities 1 & 2 is -0.6. If you combine securities #1 & #2 in a portfolio in a 30:70 ratio, what is the risk (standard deviation) of the resultant portfolio? Note: please make sure to follow convention and write all percentages as a decimal i.e. 30% = 0.3, 10% = 0.1. Complete your calculations correct to four decimal places. A. 6.50% B. 7.90% C.7.57% D. 2.42%

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock