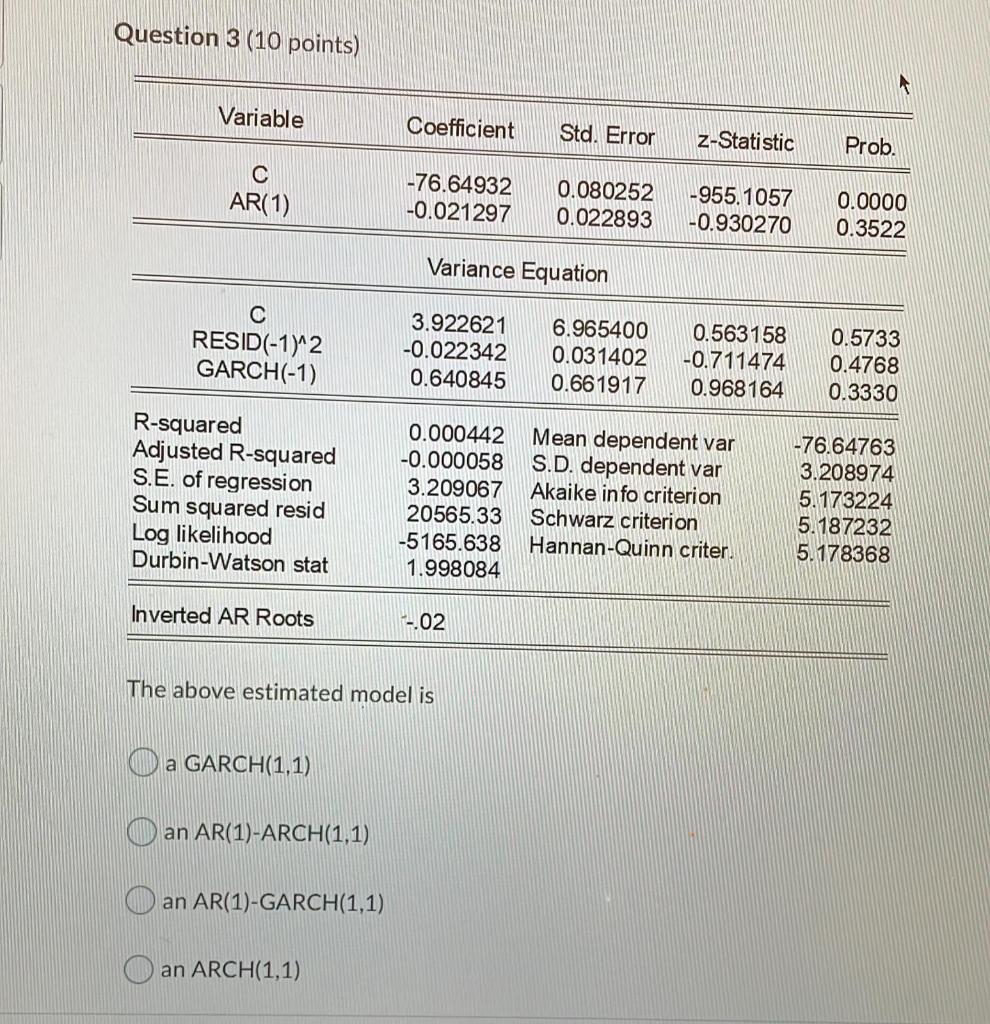

Question: Question 3 (10 points) Variable Coefficient Std. Error z-Statistic Prob. AR(1) -76.64932 -0.021297 0.080252 0.022893 -955.1057 -0.930270 0.0000 0.3522 Variance Equation C RESID(-1)^2 GARCH(-1) 3.922621

Question 3 (10 points) Variable Coefficient Std. Error z-Statistic Prob. AR(1) -76.64932 -0.021297 0.080252 0.022893 -955.1057 -0.930270 0.0000 0.3522 Variance Equation C RESID(-1)^2 GARCH(-1) 3.922621 -0.022342 0.640845 6.965400 0.031402 0.661917 0.563158 -0.711474 0.968164 0.5733 0.4768 0.3330 R-squared Adjusted R-squared S.E. of regression Sum squared resid Log likelihood Durbin-Watson stat 0.000442 -0.000058 3.209067 20565.33 -5165.638 1.998084 Mean dependent var S.D. dependent var Akaike info criterion Schwarz criterion Hannan-Quinn criter. -76.64763 3.208974 5.173224 5.187232 5.178368 Inverted AR Roots --02 The above estimated model is a GARCH(1,1) an AR(1)-ARCH(1,1) an AR(1)-GARCH(1,1) an ARCH(1,1)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts