Question: Question 3 a. Using the data in the table below and calculate the following performance measures. i. Sharpe ratio ii. Treynor measure iii. Jensen's alpha

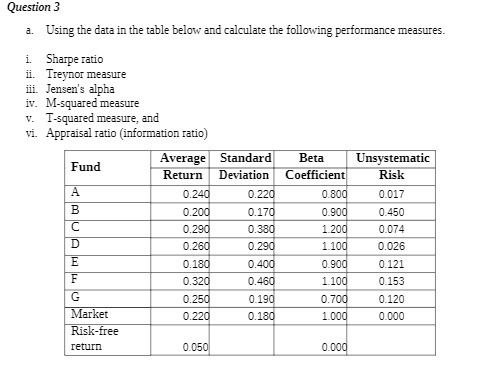

Question 3 a. Using the data in the table below and calculate the following performance measures. i. Sharpe ratio ii. Treynor measure iii. Jensen's alpha iv. M-squared measure v. T-squared measure, and vi. Appraisal ratio (information ratio) Average Standard Beta Unsystematic Fund Return Deviation Coefficient Risk A 0.240 0.220 0.800 0.017 B 0.200 0.170 0.900 0.450 C 0.290 0.380 1 200 0.074 D 0.260 0.290 1 100 0.026 E 0.180 0.400 0.900 0.121 F 0.320 0.460 1 100 0.153 G 0.250 0.190 0.700 0.120 Market 0.220 0.180 1 000 0.000 Risk-free return 0.050 0.000

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock