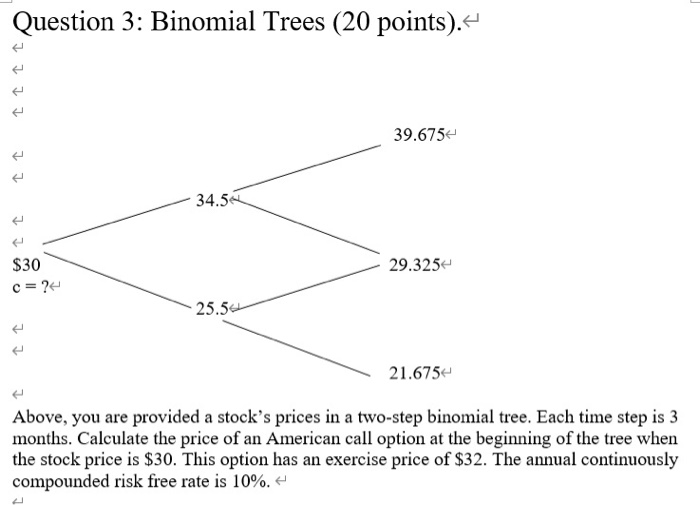

Question: Question 3: Binomial Trees (20 points). I I to 39.6754 I 34.5 29.325 $30 c=? 25.54 21.675 Above, you are provided a stock's prices in

Question 3: Binomial Trees (20 points). I I to 39.6754 I 34.5 29.325 $30 c=? 25.54 21.675 Above, you are provided a stock's prices in a two-step binomial tree. Each time step is 3 months. Calculate the price of an American call option at the beginning of the tree when the stock price is $30. This option has an exercise price of $32. The annual continuously compounded risk free rate is 10%

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock