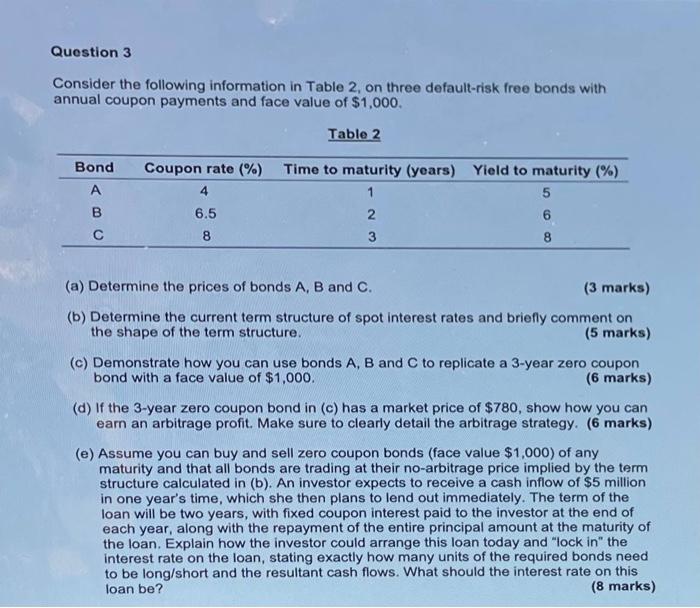

Question: Question 3 Consider the following information in Table 2 , on three default - risk free bonds with annual coupon payments and face value of

Question Consider the following information in Table on three defaultrisk free bonds with annual coupon payments and face value of $ Table Bond Coupon rate A Time to maturity years Yield to maturity a Determine the prices of bonds A B and C marksb Determine the current term structure of spot interest rates and briefly comment on the shape of the term structure. marksc Demonstrate how you can use bonds A B and C to replicate a year zero coupon bond with a face value of $ marksd If the year zero coupon bond in c has a market price of $ show how you can earn an arbitrage profit. Make sure to clearly detail the arbitrage strategy. markse Assume you can buy and sell zero coupon bonds face value $ of any maturity and that all bonds are trading at their noarbitrage price implied by the term structure calculated in b An investor expects to receive a cash inflow of $ million in one year's time, which she then plans to lend out immediately. The term of the loan will be two years, with fixed coupon interest paid to the investor at the end of each year, along with the repayment of the entire principal amount at the maturity of the loan. Explain how the investor could arrange this loan today and "lock in the interest rate on the loan, stating exactly how many units of the required bonds need to be longshort and the resultant cash flows. What should the interest rate on this loan be marks

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock