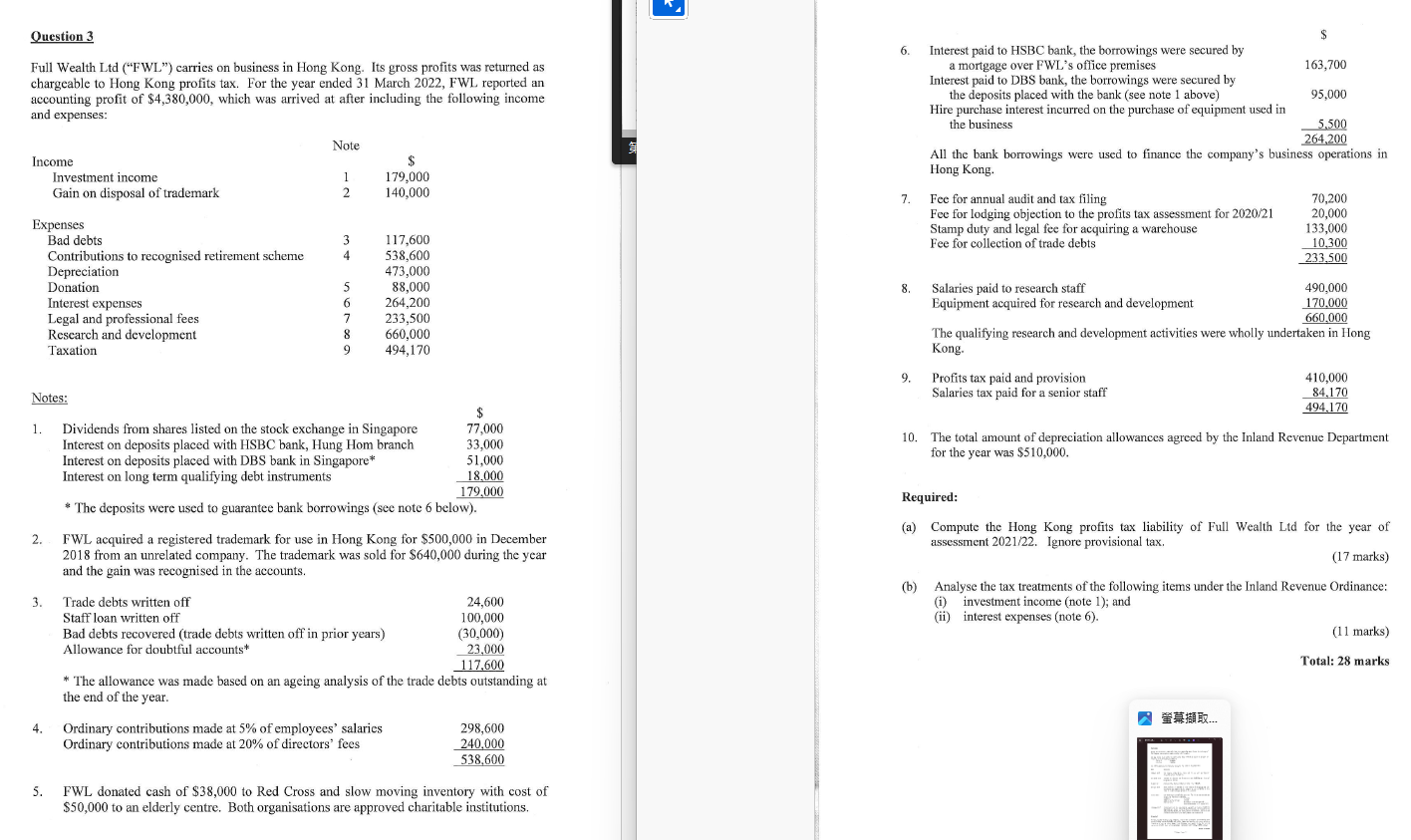

Question 3 Full Wealth Ltd (FWL) carries on business in Hong Kong. Its gross profits was...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

Question 3 Full Wealth Ltd ("FWL") carries on business in Hong Kong. Its gross profits was returned as chargeable to Hong Kong profits tax. For the year ended 31 March 2022, FWL reported an accounting profit of $4,380,000, which was arrived at after including the following income and expenses: Income Investment income Gain on disposal of trademark Note 1 179,000 2 140,000 Expenses Bad debts 3 117,600 Contributions to recognised retirement scheme 4 538,600 Depreciation 473,000 Donation 88,000 Interest expenses 6 264,200 Legal and professional fees 7 233,500 Research and development 8 660,000 Taxation 9 494,170 $ 6. Interest paid to HSBC bank, the borrowings were secured by a mortgage over FWL's office premises 163,700 Interest paid to DBS bank, the borrowings were secured by the deposits placed with the bank (see note 1 above) Hire purchase interest incurred on the purchase of equipment used in the business 95,000 5,500 264,200 All the bank borrowings were used to finance the company's business operations in Hong Kong. 7. Fee for annual audit and tax filing 70,200 Fee for lodging objection to the profits tax assessment for 2020/21 20,000 Stamp duty and legal fee for acquiring a warehouse 133,000 Fee for collection of trade debts 10,300 233,500 8. Salaries paid to research staff 490,000 Equipment acquired for research and development 170,000 660,000 Notes: 1. Dividends from shares listed on the stock exchange in Singapore Interest on deposits placed with HSBC bank, Hung Hom branch Interest on deposits placed with DBS bank in Singapore* Interest on long term qualifying debt instruments 77,000 33,000 51,000 18.000 179,000 *The deposits were used to guarantee bank borrowings (see note 6 below). 2. FWL acquired a registered trademark for use in Hong Kong for $500,000 in December 2018 from an unrelated company. The trademark was sold for $640,000 during the year and the gain was recognised in the accounts. 3. Trade debts written off 24,600 100,000 (30,000) 23,000 117,600 Staff loan written off Bad debts recovered (trade debts written off in prior years) Allowance for doubtful accounts* *The allowance was made based on an ageing analysis of the trade debts outstanding at the end of the year. The qualifying research and development activities were wholly undertaken in Hong Kong. 9. Profits tax paid and provision Salaries tax paid for a senior staff 410,000 84,170 494,170 10. The total amount of depreciation allowances agreed by the Inland Revenue Department for the year was $510,000. Required: (a) Compute the Hong Kong profits tax liability of Full Wealth Ltd for the year of assessment 2021/22. Ignore provisional tax. (17 marks) (b) Analyse the tax treatments of the following items under the Inland Revenue Ordinance: (i) investment income (note 1); and (ii) interest expenses (note 6). (11 marks) Total: 28 marks 4. Ordinary contributions made at 5% of employees' salaries Ordinary contributions made at 20% of directors' fees 5. 298,600 240,000 538,600 FWL donated cash of $38,000 to Red Cross and slow moving inventory with cost of $50,000 to an elderly centre. Both organisations are approved charitable institutions. .... Question 3 Full Wealth Ltd ("FWL") carries on business in Hong Kong. Its gross profits was returned as chargeable to Hong Kong profits tax. For the year ended 31 March 2022, FWL reported an accounting profit of $4,380,000, which was arrived at after including the following income and expenses: Income Investment income Gain on disposal of trademark Note 1 179,000 2 140,000 Expenses Bad debts 3 117,600 Contributions to recognised retirement scheme 4 538,600 Depreciation 473,000 Donation 88,000 Interest expenses 6 264,200 Legal and professional fees 7 233,500 Research and development 8 660,000 Taxation 9 494,170 $ 6. Interest paid to HSBC bank, the borrowings were secured by a mortgage over FWL's office premises 163,700 Interest paid to DBS bank, the borrowings were secured by the deposits placed with the bank (see note 1 above) Hire purchase interest incurred on the purchase of equipment used in the business 95,000 5,500 264,200 All the bank borrowings were used to finance the company's business operations in Hong Kong. 7. Fee for annual audit and tax filing 70,200 Fee for lodging objection to the profits tax assessment for 2020/21 20,000 Stamp duty and legal fee for acquiring a warehouse 133,000 Fee for collection of trade debts 10,300 233,500 8. Salaries paid to research staff 490,000 Equipment acquired for research and development 170,000 660,000 Notes: 1. Dividends from shares listed on the stock exchange in Singapore Interest on deposits placed with HSBC bank, Hung Hom branch Interest on deposits placed with DBS bank in Singapore* Interest on long term qualifying debt instruments 77,000 33,000 51,000 18.000 179,000 *The deposits were used to guarantee bank borrowings (see note 6 below). 2. FWL acquired a registered trademark for use in Hong Kong for $500,000 in December 2018 from an unrelated company. The trademark was sold for $640,000 during the year and the gain was recognised in the accounts. 3. Trade debts written off 24,600 100,000 (30,000) 23,000 117,600 Staff loan written off Bad debts recovered (trade debts written off in prior years) Allowance for doubtful accounts* *The allowance was made based on an ageing analysis of the trade debts outstanding at the end of the year. The qualifying research and development activities were wholly undertaken in Hong Kong. 9. Profits tax paid and provision Salaries tax paid for a senior staff 410,000 84,170 494,170 10. The total amount of depreciation allowances agreed by the Inland Revenue Department for the year was $510,000. Required: (a) Compute the Hong Kong profits tax liability of Full Wealth Ltd for the year of assessment 2021/22. Ignore provisional tax. (17 marks) (b) Analyse the tax treatments of the following items under the Inland Revenue Ordinance: (i) investment income (note 1); and (ii) interest expenses (note 6). (11 marks) Total: 28 marks 4. Ordinary contributions made at 5% of employees' salaries Ordinary contributions made at 20% of directors' fees 5. 298,600 240,000 538,600 FWL donated cash of $38,000 to Red Cross and slow moving inventory with cost of $50,000 to an elderly centre. Both organisations are approved charitable institutions. ....

Expert Answer:

Posted Date:

Students also viewed these accounting questions

-

The financial statements of CJ for the year to 31 March 2006 were as follows: Income statement for the year to 31 March 2006...

-

Explain the meaning of the terms emoluments, employments and office for the purposes of PAYE as you earn systems. 2. Explain the actual receipts basis of assessing the emoluments from the employment...

-

Explain the nature of stress at work Describe the health consequences of stressful work Explain how to use hardiness theory to reduce stress List three ways to use Banduras self-efficacy theory to...

-

Draft the following sentences in active voice. The defendant was attacked by the plaintiff at the beginning of the argument. It is a requirement of good writing skills that active voice be used....

-

Income statements for Fanning Company for Year 3 and Year 4 follow. FANNING COMPANY Income Statements Year 4. Sales $200,200 Year 3 $180,200 Cost of goods sold. 143,800 121,800 Selling expenses...

-

a. Consider a one-year futures contract for 1 share of a dividend paying stock. The current stock price is $60 and the risk-free interest rate is 8% p.a. It is also known that the stock will pay a $2...

-

The Justice Department sued several universities for collectively setting the size of scholarships offered. Explain why the alleged price fixing on the part of universities might be harmful to...

-

Two different computer processors are compared by measuring the processing speed for different operations performed by computers using the two processors. If 12 measurements with the first processor...

-

With reference to Exercise 8.5, test the null hypothesis that \(\sigma=0.75\) hours for the time that is required for repairs of the second type of bulldozer against the alternative hypothesis that...

-

Suppose a monopolist is practicing price discrimination and a lawsuit against the monopolist forces an end to the practice. Is it possible that the result is a loss in efficiency? Explain.

-

Past data indicate that the variance of measurements made on sheet metal stampings by experienced quality-control inspectors is 0.18 (inch) \({ }^{2}\). Such measurements made by an inexperienced...

Study smarter with the SolutionInn App