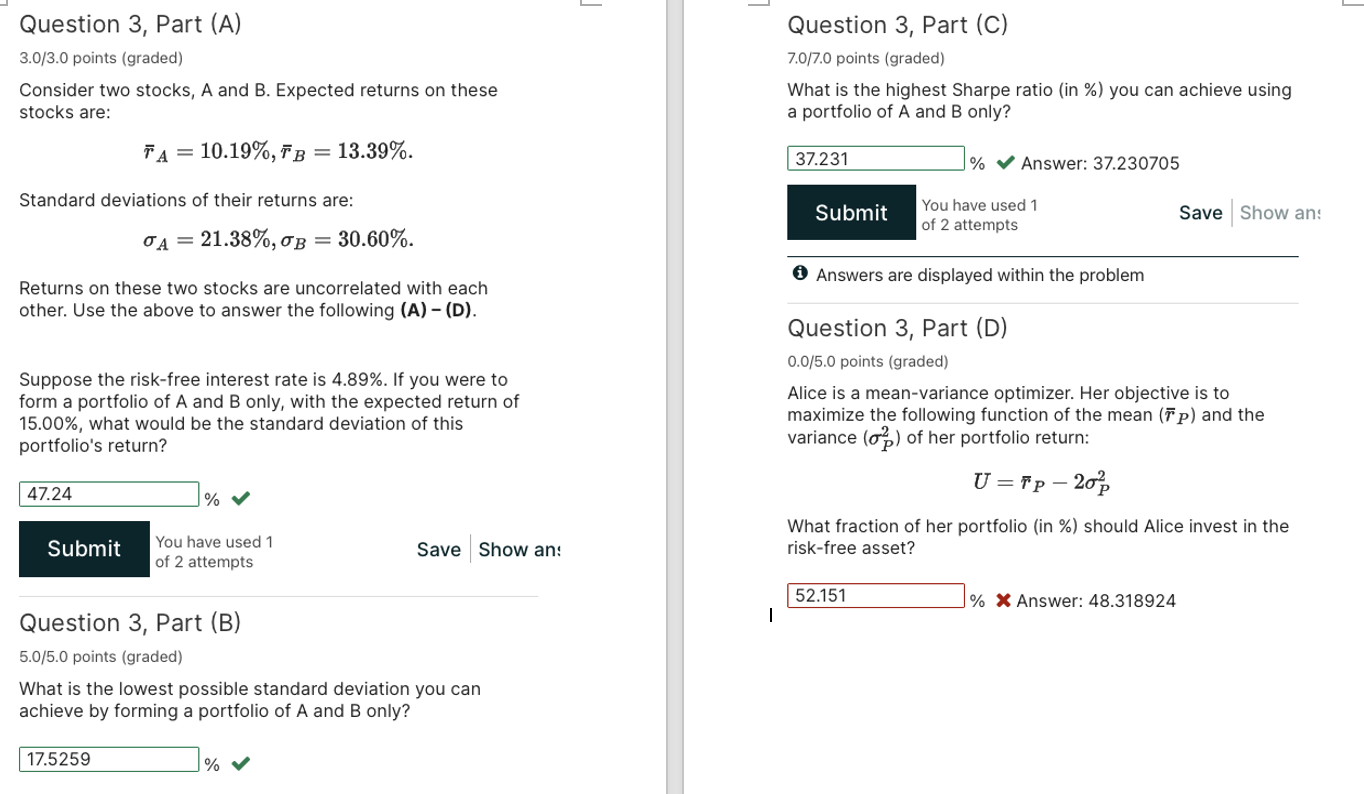

Question: Question 3, Part (A) 3.0/3.0 points (graded) Consider two stocks, A and B. Expected returns on these stocks are: TA = 10.19%, TB =

Question 3, Part (A) 3.0/3.0 points (graded) Consider two stocks, A and B. Expected returns on these stocks are: TA = 10.19%, TB = 13.39%. Standard deviations of their returns are: A=21.38%, = 30.60%. Returns on these two stocks are uncorrelated with each other. Use the above to answer the following (A) - (D). Suppose the risk-free interest rate is 4.89%. If you were to form a portfolio of A and B only, with the expected return of 15.00%, what would be the standard deviation of this portfolio's return? 47.24 % You have used 1 Submit Save Show an of 2 attempts Question 3, Part (C) 7.0/7.0 points (graded) What is the highest Sharpe ratio (in %) you can achieve using a portfolio of A and B only? 37.231 Submit % Answer: 37.230705 Save Show an You have used 1 of 2 attempts Answers are displayed within the problem Question 3, Part (D) 0.0/5.0 points (graded) Alice is a mean-variance optimizer. Her objective is to maximize the following function of the mean (rp) and the variance (a) of her portfolio return: U-p-20 What fraction of her portfolio (in %) should Alice invest in the risk-free asset? Question 3, Part (B) 5.0/5.0 points (graded) What is the lowest possible standard deviation you can achieve by forming a portfolio of A and B only? 17.5259 % 52.151 I % Answer: 48.318924

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts