Question: Question (31) (a) Which stock has the most significant beta estimate and why? The greater Absolute t-Stat so Firm B (b) If Covariance ( (A,

Question (31) (a) Which stock has the most significant beta estimate and why? The greater Absolute t-Stat so Firm B (b) If Covariance ( (A, B)=136.6 ) (expressed in %), what is the standard deviation of the market? ( operatorname{Cov}(A B) ) (c) If Variance ( (A)=158 ) (expressed in %), what is the firm-specific standard deviation of firm A stock? (d) If Variance ( (B)=255.6 ) (expressed in %); find the R-square of the portfolio that has ( 75 % ) weight in ( A ) and ( 25 % ) weight in ( B )

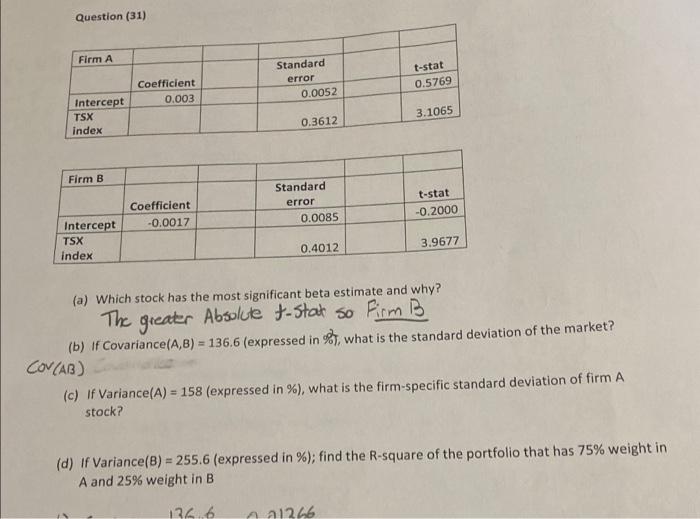

Question (31) (a) Which stock has the most significant beta estimate and why? The greater Absolute t-Stat so Firm B (b) If Covariance (A,B)=136.6 (expressed in \%), what is the standard deviation of the market? cov(AB) (c) If Variance (A)=158 (expressed in \%), what is the firm-specific standard deviation of firm A stock? (d) If Variance(B) =255.6 (expressed in \%); find the R-square of the portfolio that has 75% weight in A and 25% weight in B

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock