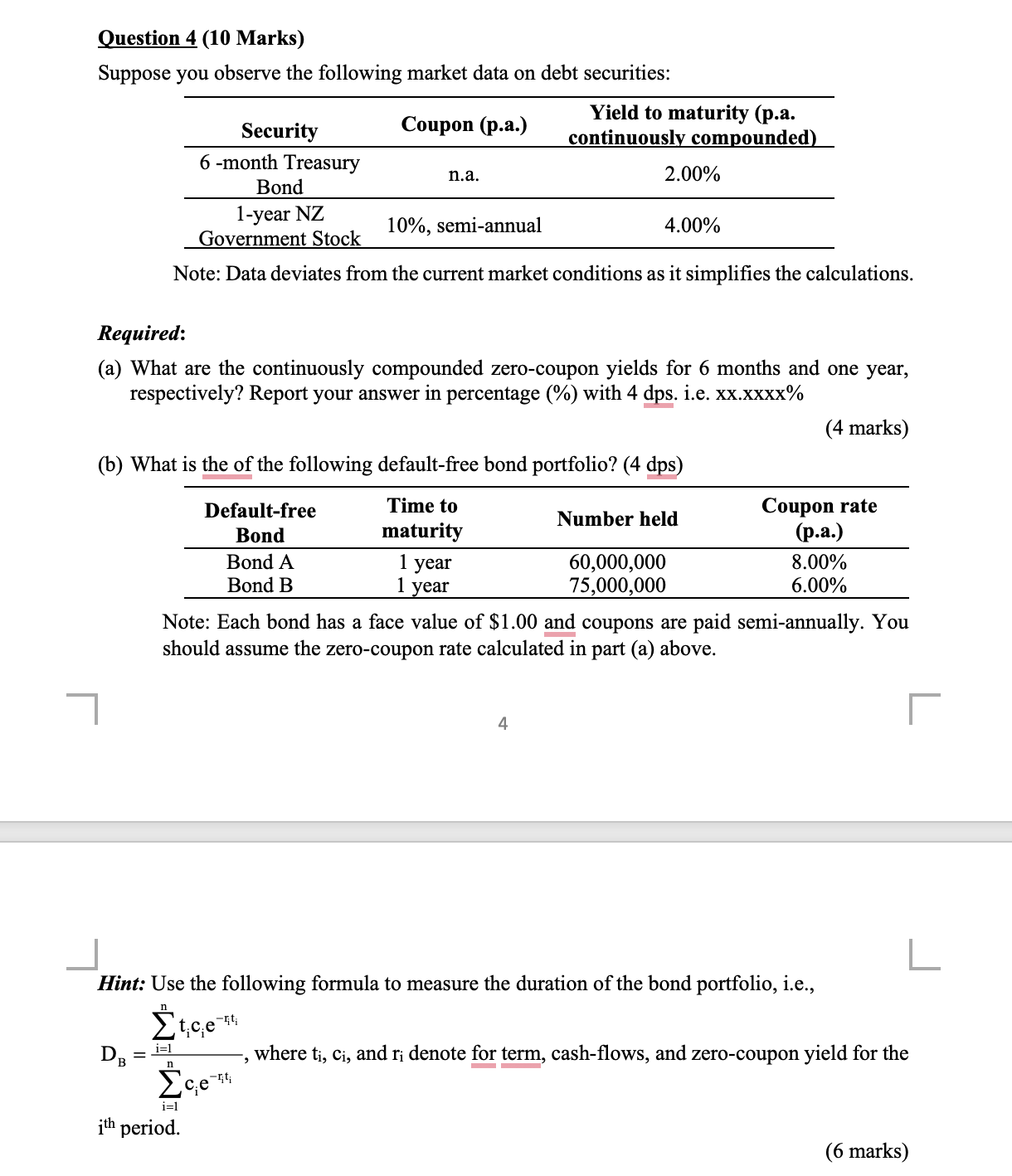

Question: Question 4 ( 1 0 Marks ) Suppose you observe the following market data on debt securities: Note: Data deviates from the current market conditions

Question Marks

Suppose you observe the following market data on debt securities:

Note: Data deviates from the current market conditions as it simplifies the calculations.

Required:

a What are the continuously compounded zerocoupon yields for months and one year,

respectively? Report your answer in percentage with dps ie

b What is the of the following defaultfree bond portfolio? dps

Note: Each bond has a face value of $ and coupons are paid semiannually. You

should assume the zerocoupon rate calculated in part a above.

Hint: Use the following formula to measure the duration of the bond portfolio, ie

period.

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock