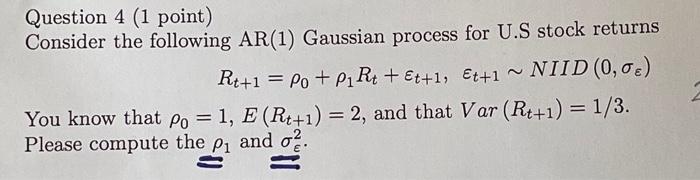

Question: Question 4 (1 point) Consider the following AR(1) Gaussian process for U.S stock returns Rt+1 = Po + P Rt + Et+1, Et+1 ~ NIID

Question 4 (1 point) Consider the following AR(1) Gaussian process for U.S stock returns Rt+1 = Po + P Rt + Et+1, Et+1 ~ NIID (0,0%) You know that po = 1, E (Rt+1) = 2, and that Var (Rt+1) = 1/3. Please compute the p and .

Question 4 (1 point) Consider the following AR(1) Gaussian process for U.S stock returns Rt+1=0+1Rt+t+1,t+1NIID(0,) You know that 0=1,E(Rt+1)=2, and that Var(Rt+1)=1/3. Please compute the 1 and 2

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock