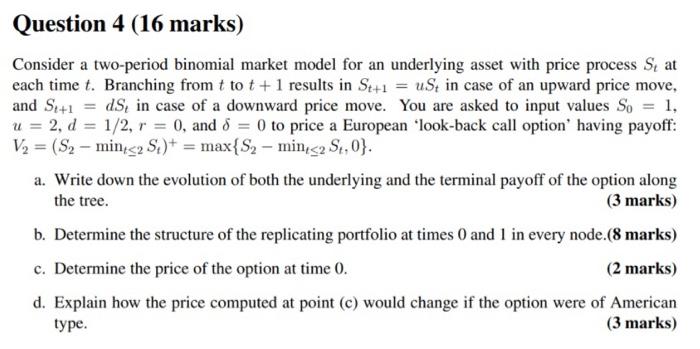

Question: Question 4 (16 marks) Consider a two-period binomial market model for an underlying asset with price process Se at each time t. Branching from t

Question 4 (16 marks) Consider a two-period binomial market model for an underlying asset with price process Se at each time t. Branching from t to t +1 results in St+1 = ust in case of an upward price move, and Se+1 = ds, in case of a downward price move. You are asked to input values So = 1, u = 2, d = 1/2, r = 0, and 8 = 0 to price a European look-back call option' having payoff: V2 = (S2 - min

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock