Question: Question 4 (20 marks) A portfolio manager observed the performance of two (2) stocks in his portfolio over a four year period. The data collected

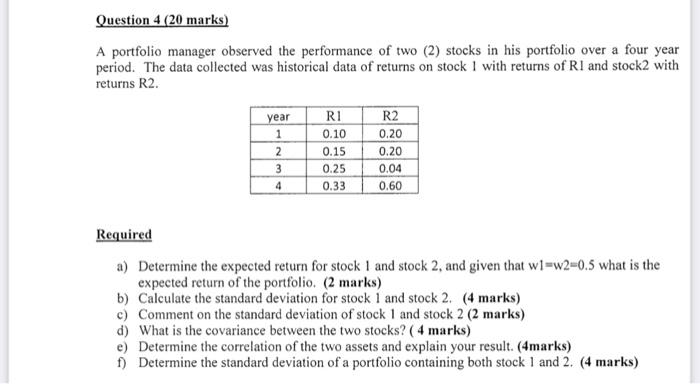

Question 4 (20 marks) A portfolio manager observed the performance of two (2) stocks in his portfolio over a four year period. The data collected was historical data of returns on stock 1 with returns of R1 and stock2 with returns R2. year RI R2 1 0.10 0.20 2 0.15 0.20 3 0.25 0.04 4 0.33 0.60 Required a) Determine the expected return for stock 1 and stock 2, and given that wl=w2-0.5 what is the expected return of the portfolio. (2 marks) b) Calculate the standard deviation for stock 1 and stock 2. (4 marks) c) Comment on the standard deviation of stock 1 and stock 2 (2 marks) d) What is the covariance between the two stocks? (4 marks) e) Determine the correlation of the two assets and explain your result. (4marks) f) Determine the standard deviation of a portfolio containing both stock 1 and 2. (4 marks)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts