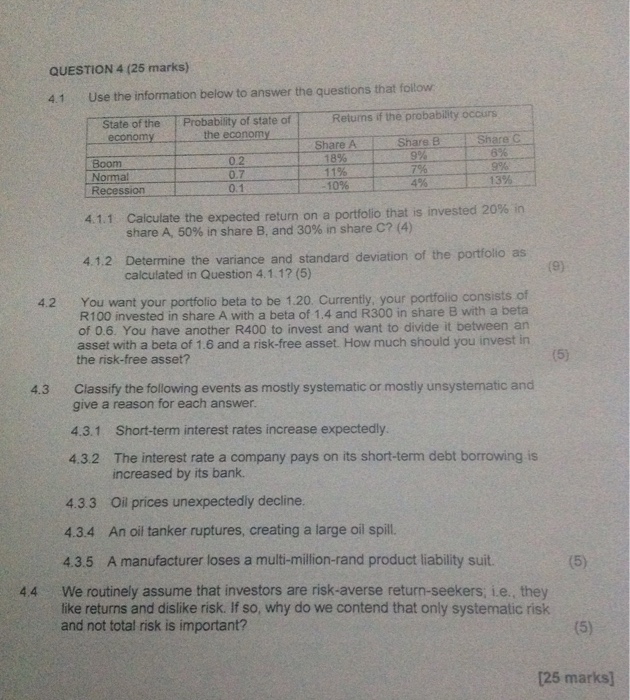

Question: QUESTION 4 (25 marks) 4.1 Use the information below to answer the questions that follow State of the Probability of state ofReturns if the economy

QUESTION 4 (25 marks) 4.1 Use the information below to answer the questions that follow State of the Probability of state ofReturns if the economy the probability occurs economy Share B Boom Normal Recession 0.2 0.7 0.1 Share A 18% 11% 10% 9% 13% 4% Calculate the expected return on a portfolio that is invested 20% in Share A, 50% in share B, and 30% in share C? (4) 4.1.1 Determine the variance and standard deviation of the portfolio as calculated in Question 4.1.1? (5) 4.1.2 4.2 You want your portfolio beta to be 1.20. Currently, your portfolio consists of R100 invested in share A with a beta of 1.4 and R300 in share B with a beta of 0.6. You have another R400 to invest and want to divide it between an asset with a beta of 1.6 and a risk-free asset. How much should you invest in the risk-free asset? Classify the following events as mostly systematic or mostly unsystematic and give a reason for each answer 4.3 4.3.1 Short-term interest rates increase expectedly. The interest rate a company pays on its short-term debt borrowing is increased by its bank 4.3.2 4.33 Oil prices unexpectedly decline 4.3.4 An oil tanker ruptures, creating a large oil spill. 4.3.5 A manufacturer loses a multi-million-rand product liability suit 4.4 We routinely assume that investors are risk-averse return-seekers, ie., they like returns and dislike risk. If so, why do we contend that only systematic risk and not total risk is important? 125 marks)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts