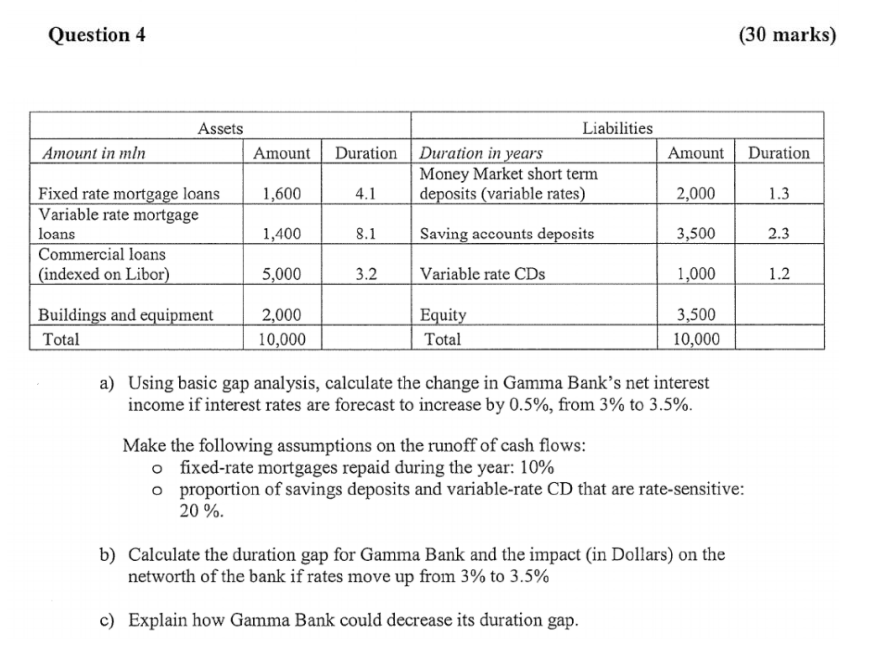

Question: Question 4 (30 marks) Assets Amount Amount in mln Liabilities Duration Duration in years Amount Money Market short term 4.1 deposits (variable rates) 2,000 Duration

Question 4 (30 marks) Assets Amount Amount in mln Liabilities Duration Duration in years Amount Money Market short term 4.1 deposits (variable rates) 2,000 Duration 1,600 1.3 Fixed rate mortgage loans Variable rate mortgage loans Commercial loans (indexed on Libor) 1,400 8.1 Saving accounts deposits 3,500 2.3 5,000 3.2 Variable rate CDs 1,000 1.2 Buildings and equipment Total 2,000 10,000 Equity Total 3,500 10,000 a) Using basic gap analysis, calculate the change in Gamma Bank's net interest income if interest rates are forecast to increase by 0.5%, from 3% to 3.5%. Make the following assumptions on the runoff of cash flows: o fixed-rate mortgages repaid during the year: 10% o proportion of savings deposits and variable-rate CD that are rate-sensitive: 20%. b) Calculate the duration gap for Gamma Bank and the impact (in Dollars) on the networth of the bank if rates move up from 3% to 3.5% c) Explain how Gamma Bank could decrease its duration gap. Question 4 (30 marks) Assets Amount Amount in mln Liabilities Duration Duration in years Amount Money Market short term 4.1 deposits (variable rates) 2,000 Duration 1,600 1.3 Fixed rate mortgage loans Variable rate mortgage loans Commercial loans (indexed on Libor) 1,400 8.1 Saving accounts deposits 3,500 2.3 5,000 3.2 Variable rate CDs 1,000 1.2 Buildings and equipment Total 2,000 10,000 Equity Total 3,500 10,000 a) Using basic gap analysis, calculate the change in Gamma Bank's net interest income if interest rates are forecast to increase by 0.5%, from 3% to 3.5%. Make the following assumptions on the runoff of cash flows: o fixed-rate mortgages repaid during the year: 10% o proportion of savings deposits and variable-rate CD that are rate-sensitive: 20%. b) Calculate the duration gap for Gamma Bank and the impact (in Dollars) on the networth of the bank if rates move up from 3% to 3.5% c) Explain how Gamma Bank could decrease its duration gap

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts