Question: QUESTION 4: [{{4 x 1} + 1) + (1 +1 +1 +1 + 1) = 10 Marks] A. The following data, relating to the performance

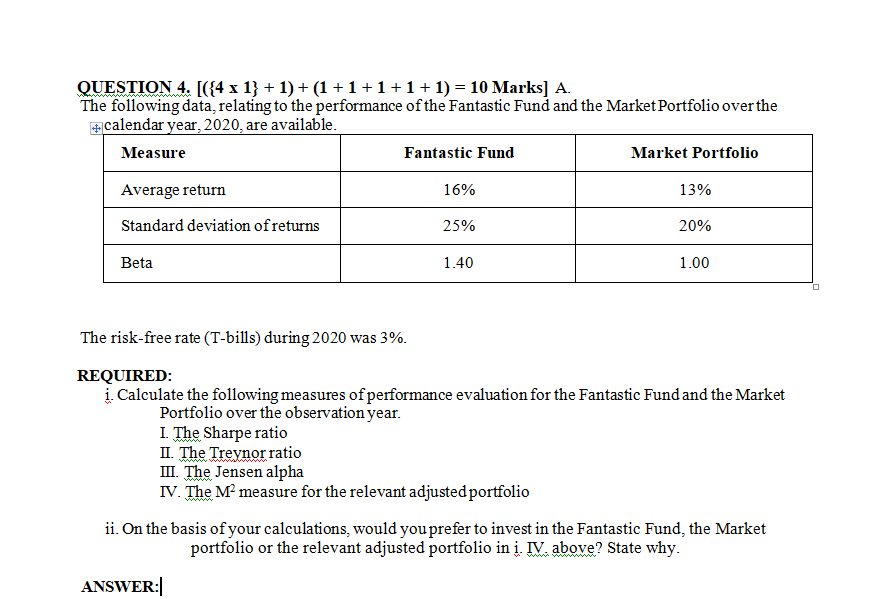

QUESTION 4: [{{4 x 1} + 1) + (1 +1 +1 +1 + 1) = 10 Marks] A. The following data, relating to the performance of the Fantastic Fund and the Market Portfolio over the calendar year, 2020, are available. Measure Fantastic Fund Market Portfolio Average return 16% 13% Standard deviation of returns 25% 20% Beta 1.40 1.00 The risk-free rate (T-bills) during 2020 was 3%. REQUIRED: 1. Calculate the following measures of performance evaluation for the Fantastic Fund and the Market Portfolio over the observation year. I The Sharpe ratio II. The Treynor ratio III. The Jensen alpha IV. The Mmeasure for the relevant adjusted portfolio ii. On the basis of your calculations, would you prefer to invest in the Fantastic Fund, the Market portfolio or the relevant adjusted portfolio in i. IV. above? State why

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts