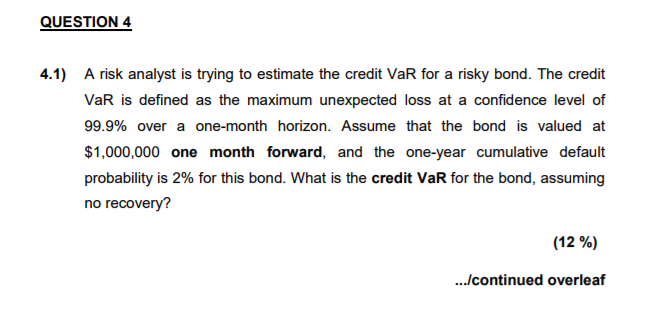

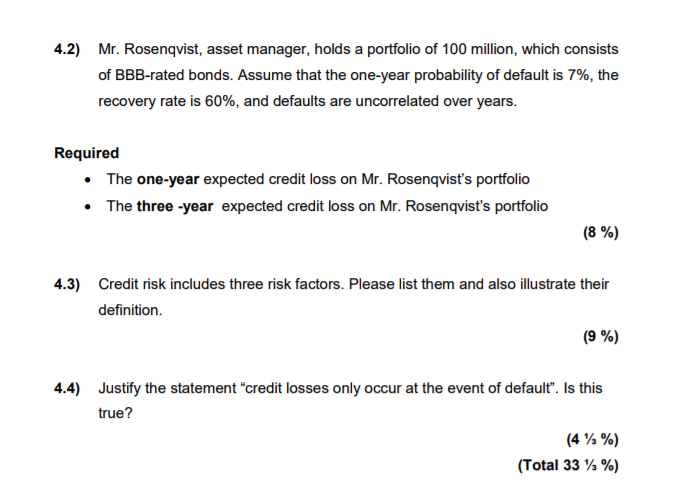

Question: QUESTION 4 4.1) A risk analyst is trying to estimate the credit VaR for a risky bond. The credit VaR is defined as the maximum

QUESTION 4 4.1) A risk analyst is trying to estimate the credit VaR for a risky bond. The credit VaR is defined as the maximum unexpected loss at a confidence level of 99.9% over a one-month horizon. Assume that the bond is valued at $1,000,000 one month forward, and the one-year cumulative default no recovery? (12 %) .../continue d overleaf QUESTION 4 4.1) A risk analyst is trying to estimate the credit VaR for a risky bond. The credit VaR is defined as the maximum unexpected loss at a confidence level of 99.9% over a one-month horizon. Assume that the bond is valued at $1,000,000 one month forward, and the one-year cumulative default no recovery? (12 %) .../continue d overleaf

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts