Question: Question 4 (5 Points): The Value at Risk ( VaR ) is a statistical measure that estimates the maximum amount of money an investor can

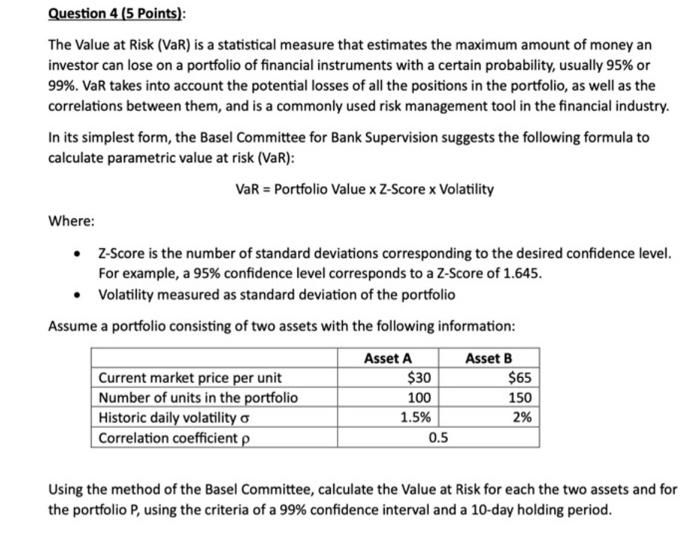

Question 4 (5 Points): The Value at Risk ( VaR ) is a statistical measure that estimates the maximum amount of money an investor can lose on a portfolio of financial instruments with a certain probability, usually 95% or 99%. VaR takes into account the potential losses of all the positions in the portfolio, as well as the correlations between them, and is a commonly used risk management tool in the financial industry. In its simplest form, the Basel Committee for Bank Supervision suggests the following formula to calculate parametric value at risk (VaR) : VaR=PortfolioValueZ-ScoreVolatility Where: - Z-Score is the number of standard deviations corresponding to the desired confidence level. For example, a 95% confidence level corresponds to a Z-Score of 1.645 . - Volatility measured as standard deviation of the portfolio Assume a portfolio consisting of two assets with the following information: Using the method of the Basel Committee, calculate the Value at Risk for each the two assets and for the portfolio P, using the criteria of a 99% confidence interval and a 10-day holding period

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts