Question: QUESTION 4 On 1 July 2019, P Ltd. acquired a 75% equity stake in S Ltd. for $160,000 and a 5% equity stake in

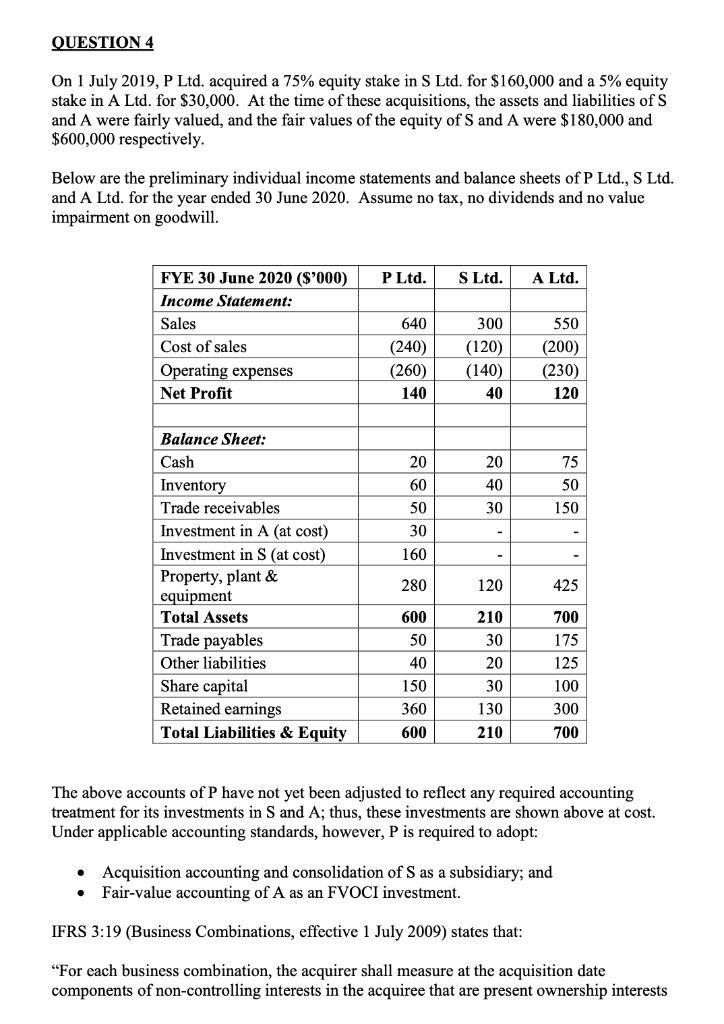

QUESTION 4 On 1 July 2019, P Ltd. acquired a 75% equity stake in S Ltd. for $160,000 and a 5% equity stake in A Ltd. for $30,000. At the time of these acquisitions, the assets and liabilities of S and A were fairly valued, and the fair values of the equity of S and A were $180,000 and $600,000 respectively. Below are the preliminary individual income statements and balance sheets of P Ltd., S Ltd. and A Ltd. for the year ended 30 June 2020. Assume no tax, no dividends and no value impairment on goodwill. FYE 30 June 2020 ($'000) P Ltd. S Ltd. A Ltd. Income Statement: Sales 640 300 550 Cost of sales (240) (120) (200) Operating expenses (260) (140) (230) Net Profit 140 40 120 Balance Sheet: Cash 20 20 75 Inventory 60 40 50 Trade receivables 50 30 150 Investment in A (at cost) 30 Investment in S (at cost) 160 Property, plant & 280 120 425 equipment Total Assets 600 210 700 Trade payables Other liabilities 50 30 175 40 20 125 Share capital 150 30 100 Retained earnings 360 130 300 Total Liabilities & Equity 600 210 700 The above accounts of P have not yet been adjusted to reflect any required accounting treatment for its investments in S and A; thus, these investments are shown above at cost. Under applicable accounting standards, however, P is required to adopt: Acquisition accounting and consolidation of S as a subsidiary; and Fair-value accounting of A as an FVOCI investment. IFRS 3:19 (Business Combinations, effective 1 July 2009) states that: "For each business combination, the acquirer shall measure at the acquisition date components of non-controlling interests in the acquiree that are present ownership interests

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts