Question: Question 4 please, not Q3 3. Your have decided to invest all your wealth in two mutual funds: A and B. Their returns are characterized

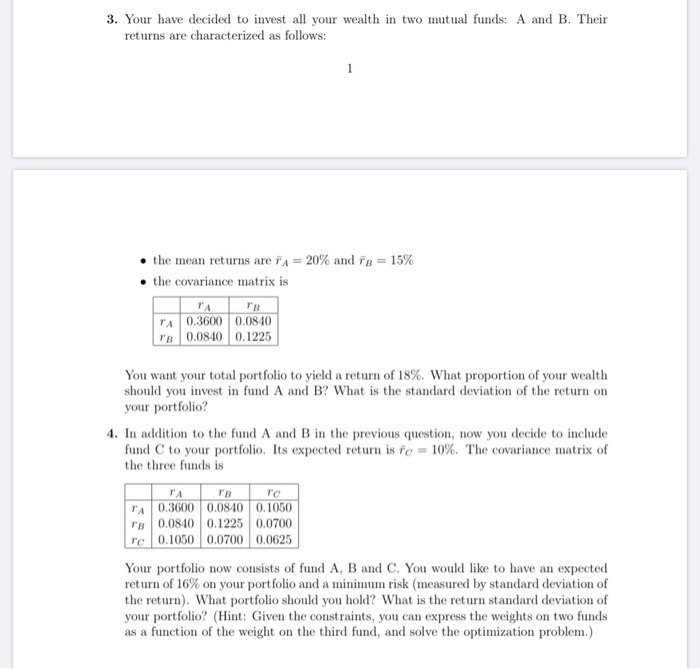

3. Your have decided to invest all your wealth in two mutual funds: A and B. Their returns are characterized as follows: the mean returns are A = 20% and is = 15% the covariance matrix is A 0.3600 0.0840 B 0.0840 0.1225 You want your total portfolio to yield a return of 18%. What proportion of your wealth should you invest in fund A and B? What is the standard deviation of the return on your portfolio? 4. In addition to the fund A and B in the previous question, now you decide to include fund to your portfolio. Its expected return is rc = 10%. The covariance matrix of the three funds is PA 0.3600 0.0840 0.1050 B 0.0840 0.1225 0.0700 rc | 0.1050 | 0.0700 | 0.0625 Your portfolio now consists of fund A, B and C. You would like to have an expected return of 16% on your portfolio and a minimum risk (measured by standard deviation of the return). What portfolio should you hold? What is the return standard deviation of your portfolio? (Hint: Given the constraints, you can express the weights on two funds as a function of the weight on the third fund, and solve the optimization problem.)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts