Question: Question 41 (1 point) Using the Black-Scholes Formula for nondividend-paying stock determine the price of a call option given the information below. Use the cumulative

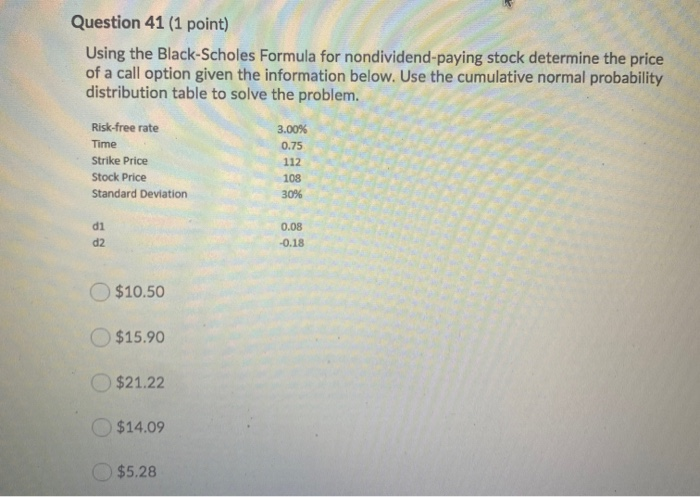

Question 41 (1 point) Using the Black-Scholes Formula for nondividend-paying stock determine the price of a call option given the information below. Use the cumulative normal probability distribution table to solve the problem. Risk-free rate 3.00% Time Strike Price Stock Price Standard Deviation 0.75 112 108 30% di d2 0.08 -0.18 $10.50 $15.90 $21.22 $14.09 $5.28

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock