Question: Question 5 ( 1 point ) Suppose you are the money manager of a million dollar investment fund. The fund consists of four stocks with

Question point

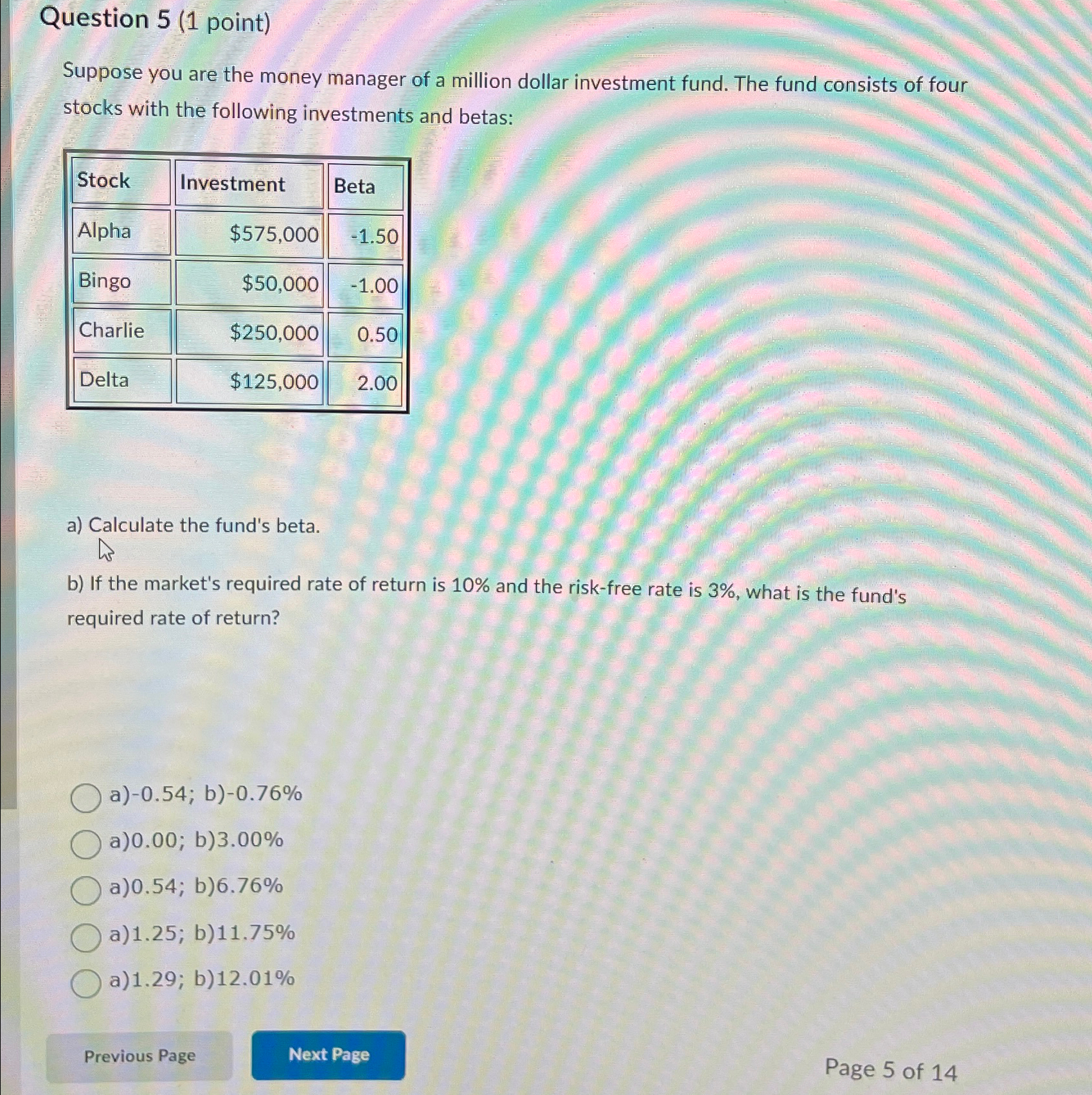

Suppose you are the money manager of a million dollar investment fund. The fund consists of four stocks with the following investments and betas:

tableStockInvestment,BetaAlpha$Bingo$Charlie$Delta$

a Calculate the fund's beta.

b If the market's required rate of return is and the riskfree rate is what is the fund's required rate of return?

a ; b

a ; b

a ; b

a ; b

a ; b

Page of

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock