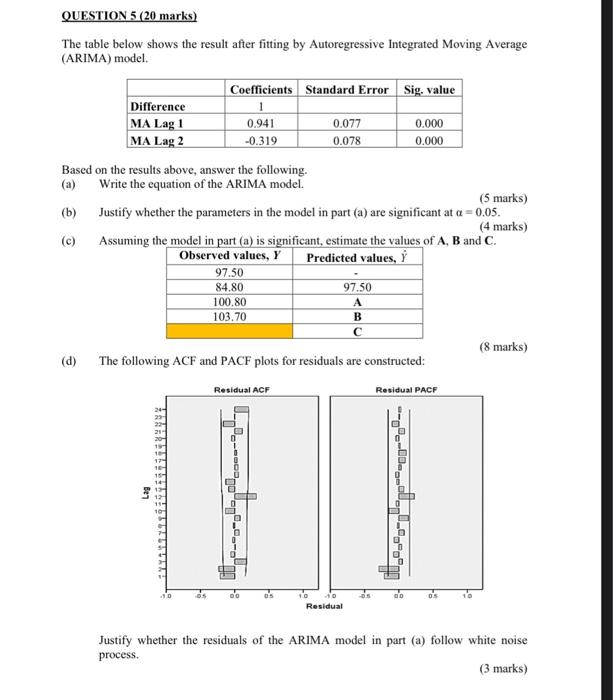

Question: QUESTION 5 (20 marks) The table below shows the result after fitting by Autoregressive Integrated Moving Average (ARIMA) model. Coefficients Standard Error Sig, value Difference

QUESTION 5 (20 marks) The table below shows the result after fitting by Autoregressive Integrated Moving Average (ARIMA) model. Coefficients Standard Error Sig, value Difference 1 MA Lag 1 0.941 0.077 0.000 MA Lag 2 -0.319 0.078 0.000 Based on the results above, answer the following. (a) Write the equation of the ARIMA model. (5 marks) (b) Justify whether the parameters in the model in part (a) are significant at a = 0.05. (4 marks) (c) Assuming the model in part (a) is significant, estimate the values of A, B and C. Observed values, Y Predicted values, Y 97.50 84.80 97.50 100.80 A 103.70 B (8 marks) (d) The following ACF and PACF plots for residuals are constructed: Residual ACF Residual PACF 15 14 Be7 00 os 05 Residual Justify whether the residuals of the ARIMA model in part (a) follow white noise process. (3 marks) QUESTION 5 (20 marks) The table below shows the result after fitting by Autoregressive Integrated Moving Average (ARIMA) model. Coefficients Standard Error Sig, value Difference 1 MA Lag 1 0.941 0.077 0.000 MA Lag 2 -0.319 0.078 0.000 Based on the results above, answer the following. (a) Write the equation of the ARIMA model. (5 marks) (b) Justify whether the parameters in the model in part (a) are significant at a = 0.05. (4 marks) (c) Assuming the model in part (a) is significant, estimate the values of A, B and C. Observed values, Y Predicted values, Y 97.50 84.80 97.50 100.80 A 103.70 B (8 marks) (d) The following ACF and PACF plots for residuals are constructed: Residual ACF Residual PACF 15 14 Be7 00 os 05 Residual Justify whether the residuals of the ARIMA model in part (a) follow white noise process

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts