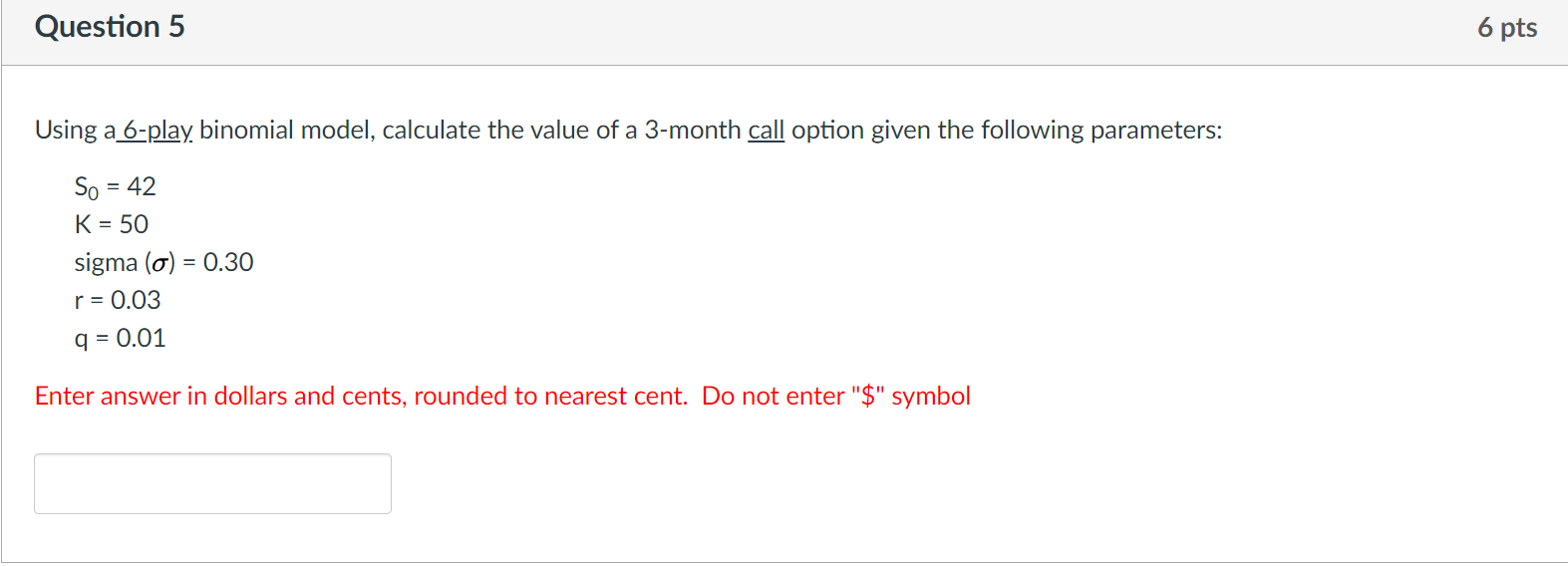

Question: Question 5 6 pts Using a 6-play binomial model, calculate the value of a 3-month call option given the following parameters: So = 42 K

Question 5 6 pts Using a 6-play binomial model, calculate the value of a 3-month call option given the following parameters: So = 42 K = 50 sigma (o) = 0.30 r = 0.03 q = 0.01 Enter answer in dollars and cents, rounded to nearest cent. Do not enter "$" symbol Question 5 6 pts Using a 6-play binomial model, calculate the value of a 3-month call option given the following parameters: So = 42 K = 50 sigma (o) = 0.30 r = 0.03 q = 0.01 Enter answer in dollars and cents, rounded to nearest cent. Do not enter "$" symbol

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock