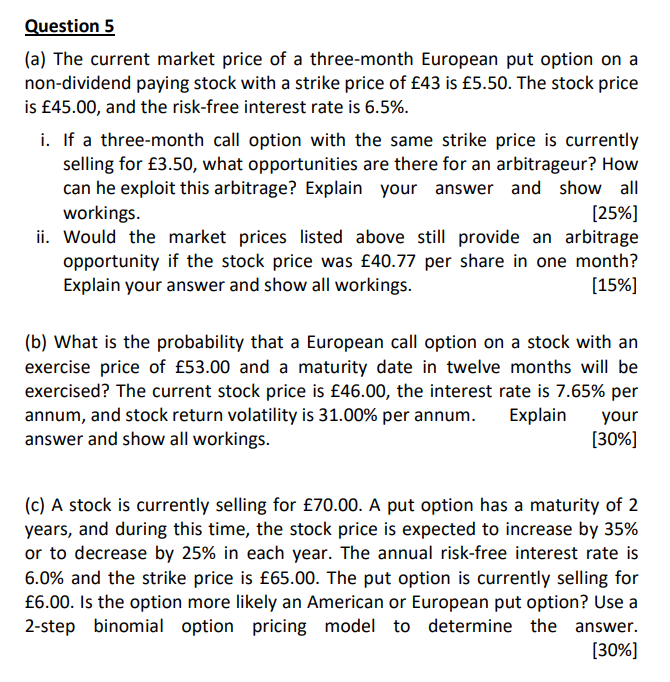

Question 5 (a) The current market price of a three-month European put option on a non-dividend...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

The image shows a financerelated question which includes three parts a b and c Each part contains a problem about options pricing and asks to determine opportunities for arbitrage probabilities of exe... View the full answer

Related Book For

Posted Date: