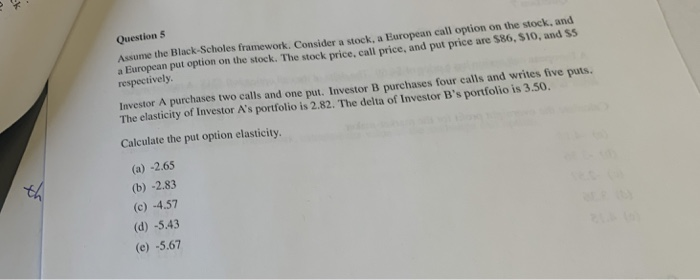

Question: Question 5 Assume the Black-Scholes framework. Consider a stock, a European call option on the stock, and respectively Investor A purchases two calls and one

Question 5 Assume the Black-Scholes framework. Consider a stock, a European call option on the stock, and respectively Investor A purchases two calls and one put. Investor B purchases four calls and writes five puts. a European put otion onthe stock. The stock price, call price, and put price are $86, $10, and ss The elasticity of Investor A's portfolio is 2.82. The delta of Investor B's portfolio is 3.50. Calculate the put option elasticity. (a) -2.65 (b) -2.83 (c) -4.57 (d) -5.43 (e) -5.67 Question 5 Assume the Black-Scholes framework. Consider a stock, a European call option on the stock, and respectively Investor A purchases two calls and one put. Investor B purchases four calls and writes five puts. a European put otion onthe stock. The stock price, call price, and put price are $86, $10, and ss The elasticity of Investor A's portfolio is 2.82. The delta of Investor B's portfolio is 3.50. Calculate the put option elasticity. (a) -2.65 (b) -2.83 (c) -4.57 (d) -5.43 (e) -5.67

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts