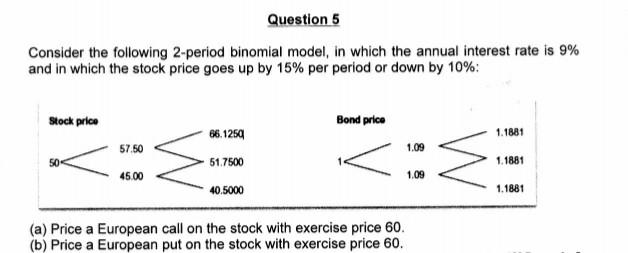

Question: Question 5 Consider the following 2-period binomial model, in which the annual interest rate is 9% and in which the stock price goes up by

Question 5 Consider the following 2-period binomial model, in which the annual interest rate is 9% and in which the stock price goes up by 15% per period or down by 10%: Stock price Bond price 66.1250 1.1881 57.50 1.09 50 1.1881 45.00 51.7500 40.5000 1.09 1.1881 (a) Price a European call on the stock with exercise price 60. (b) Price a European put on the stock with exercise price 60

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock