Question: - Question 5: (Maximum 1 page) You are a market-maker and an arbitrageur in the forward market. An asset is trading for $120 and $110

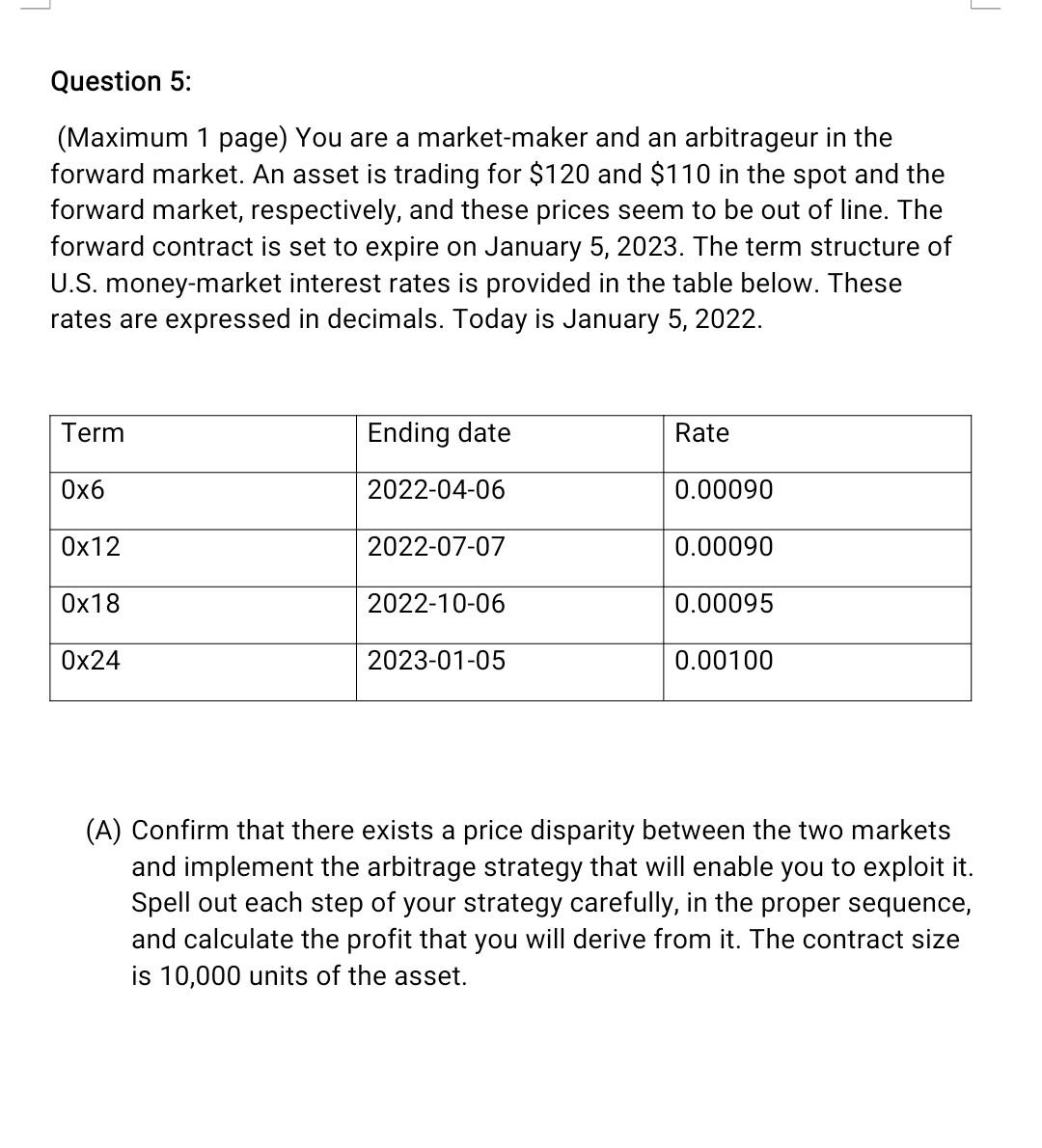

- Question 5: (Maximum 1 page) You are a market-maker and an arbitrageur in the forward market. An asset is trading for $120 and $110 in the spot and the forward market, respectively, and these prices seem to be out of line. The forward contract is set to expire on January 5, 2023. The term structure of U.S. money-market interest rates is provided in the table below. These rates are expressed in decimals. Today is January 5, 2022. Term Ending date Rate Ox6 2022-04-06 0.00090 Ox12 2022-07-07 0.00090 0x18 2022-10-06 0.00095 0x24 2023-01-05 0.00100 (A) Confirm that there exists a price disparity between the two markets and implement the arbitrage strategy that will enable you to exploit it. Spell out each step of your strategy carefully, in the proper sequence, and calculate the profit that you will derive from it. The contract size is 10,000 units of the asset

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts