Question: Question 5 Multiple Choice (20 Points) 1. What is the objective of financial reporting? a. Provide information that is useful to management in making decisions.

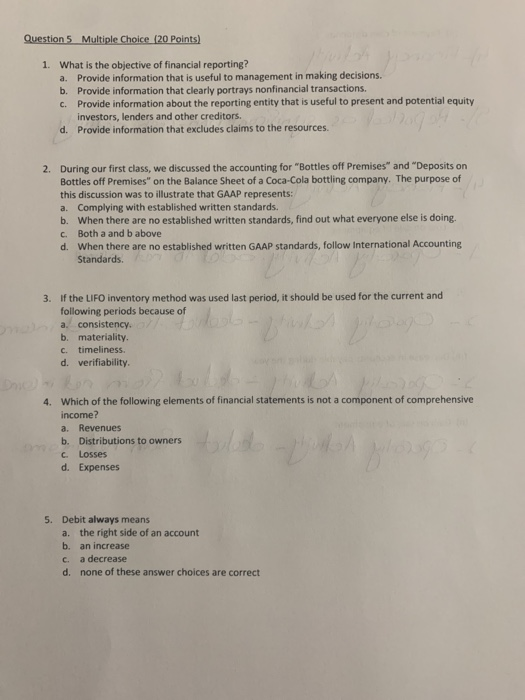

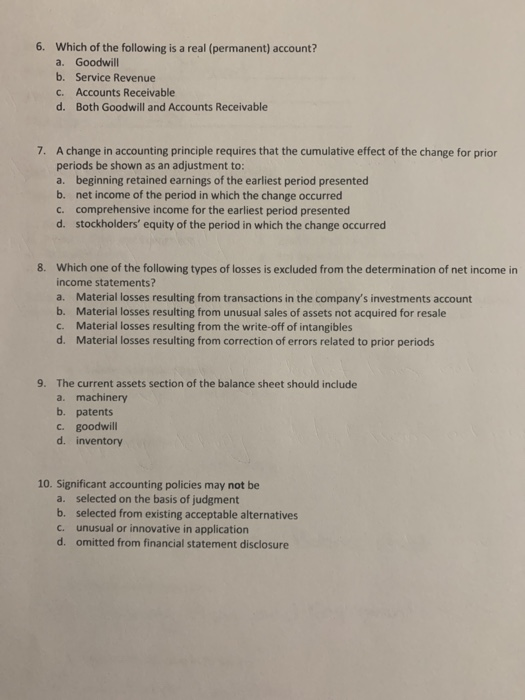

Question 5 Multiple Choice (20 Points) 1. What is the objective of financial reporting? a. Provide information that is useful to management in making decisions. b. Provide information that clearly portrays nonfinancial transactions c. Provide information about the reporting entity that is useful to present and potential equity investors, lenders and other creditors. d. Provide information that excludes claims to the resources. 2. During our first class, we discussed the accounting for "Bottles off Premises" and "Deposits on Bottles off Premises on the Balance Sheet of a Coca-Cola bottling company. The purpose of this discussion was to illustrate that GAAP represents: a. Complying with established written standards. b. When there are no established written standards, find out what everyone else is doing. c. Both a and b above d. When there are no established written GAAP standards, follow International Accounting Standards. 3. If the LIFO inventory method was used last period, it should be used for the current and following periods because of a consistency. b. materiality c. timeliness d. verifiability 4. Which of the following elements of financial statements is not a component of comprehensive income? a. Revenues b. Distributions to owners c. Losses d. Expenses 5. Debit always means a. the right side of an account b. an increase c. a decrease d. none of these answer choices are correct 6. Which of the following is a real (permanent) account? a. Goodwill b. Service Revenue C. Accounts Receivable d. Both Goodwill and Accounts Receivable 7. A change in accounting principle requires that the cumulative effect of the change for prior periods be shown as an adjustment to: a. beginning retained earnings of the earliest period presented b. net income of the period in which the change occurred C. comprehensive income for the earliest period presented d. stockholders' equity of the period in which the change occurred 8. Which one of the following types of losses is excluded from the determination of net income in income statements? a. Material losses resulting from transactions in the company's investments account b. Material losses resulting from unusual sales of assets not acquired for resale C. Material losses resulting from the write-off of intangibles d. Material losses resulting from correction of errors related to prior periods 9. The current assets section of the balance sheet should include amachinery b. patents C. goodwill d. inventory 10. Significant accounting policies may not be a. selected on the basis of judgment b. selected from existing acceptable alternatives c. unusual or innovative in application d. omitted from financial statement disclosure

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts