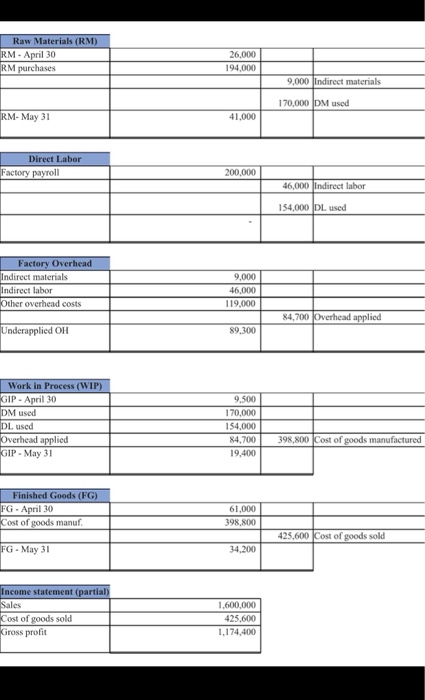

Question: Question 5 Raw Materials (RM) RM - April 30 RM purchases 26,000 194,000 9,000 Indirect materials 170,000 DM used RM-May 31 41.000 Direct Labor Factory

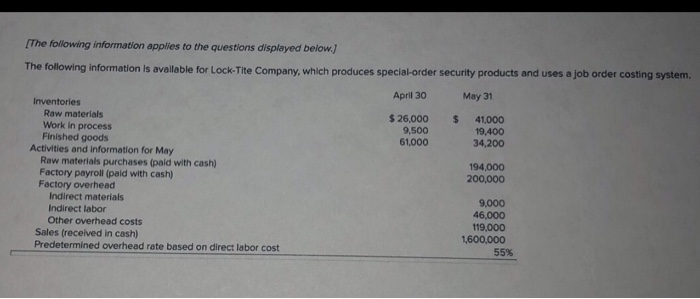

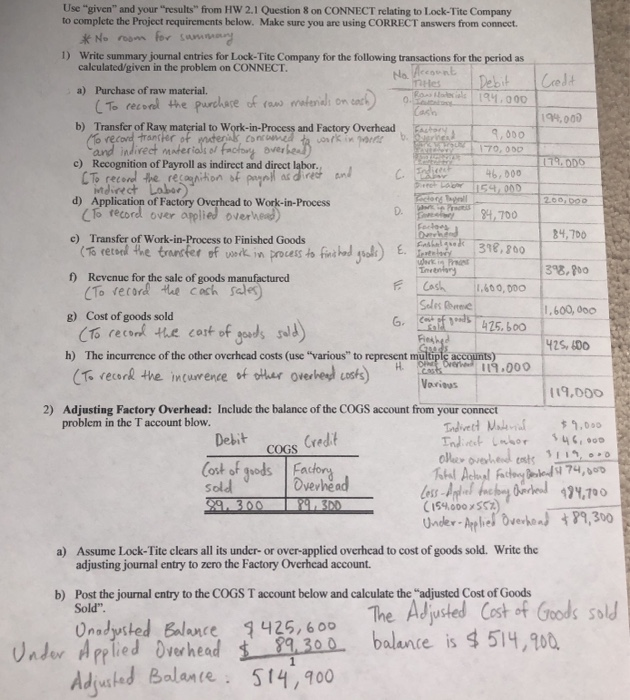

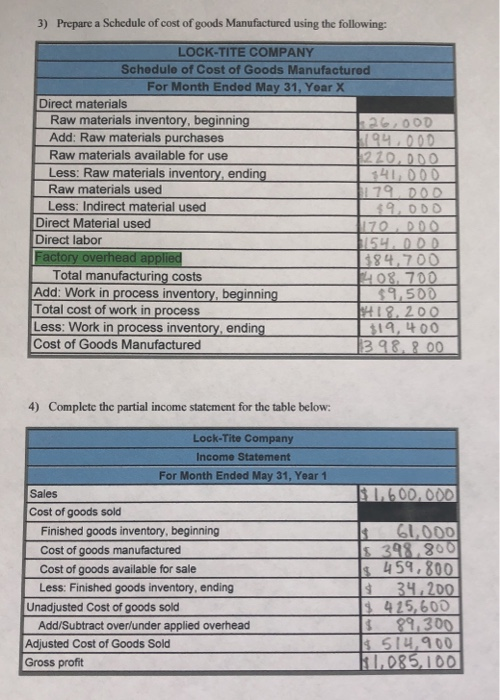

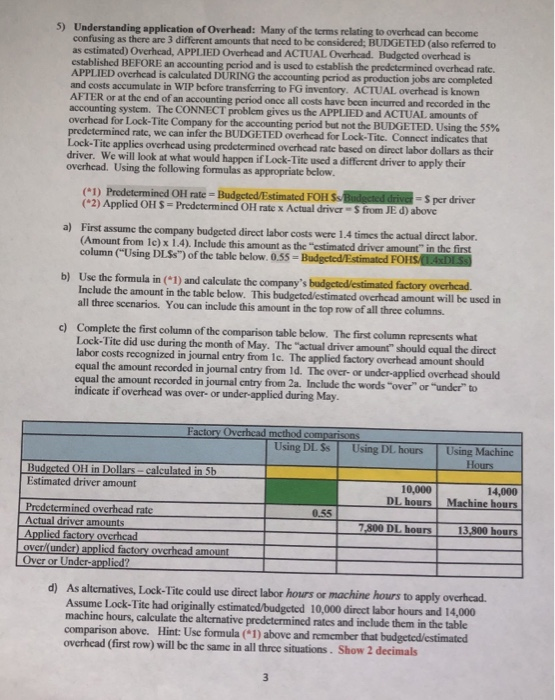

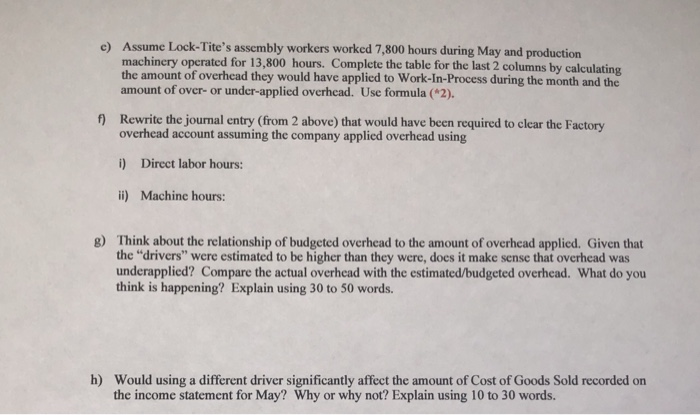

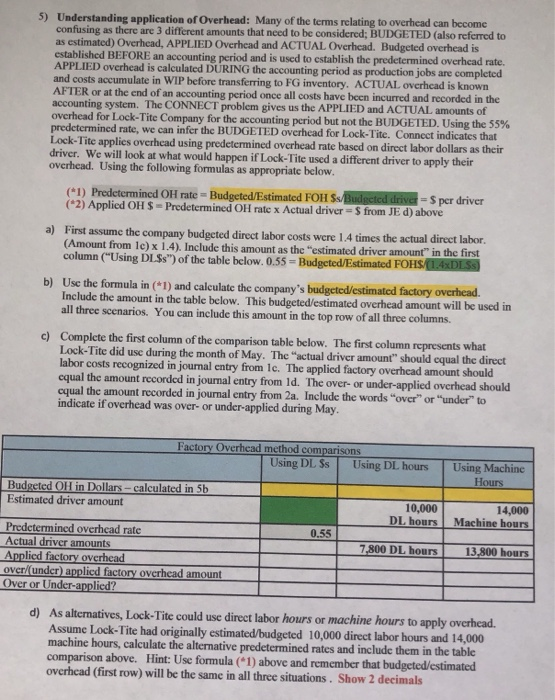

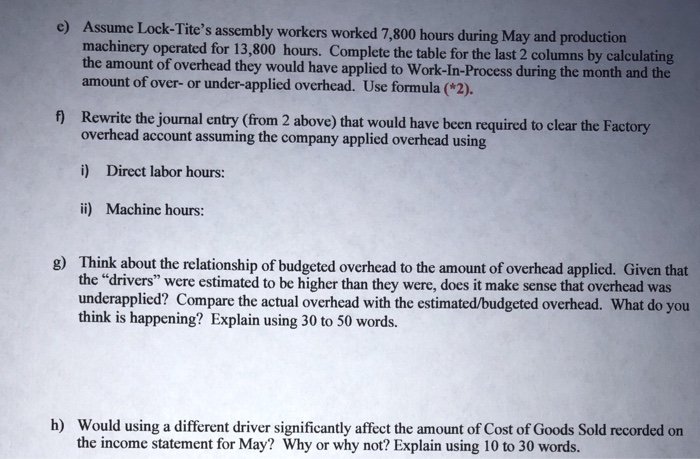

Raw Materials (RM) RM - April 30 RM purchases 26,000 194,000 9,000 Indirect materials 170,000 DM used RM-May 31 41.000 Direct Labor Factory payroll 200,000 46,000 indirect labor 154,000 DL used Factory Overhead Indirect materials Indirect labor Other overhead costs 9,000 46,000 119.000 84,700 Overhead applied Underapplied OH 89,300 Work in Process (WIP) GIP - April 30 DM used DL used Overhead applied GIP - May 31 9.500 170,000 154.000 84,700 19,400 398.800 Cost of goods manufactured Finished Goods (FG) FG - April 30 Cost of goods manuf 61.000 398,800 425,600 Cost of goods sold FG - May 31 34,200 Income statement (partial) Sales Cost of goods sold Gross profit 1,600,000 425,600 1,174,400 [The following information applies to the questions displayed below.) The following information is available for Lock-Tite Company, which produces special-order security products and uses a job order costing system. April 30 May 31 Inventories Raw materials $ 26,000 $ 41,000 Work in process 9,500 19,400 Finished goods 61,000 34,200 Activities and Information for May Raw materials purchases (pald with cash) 194,000 Factory payroll (paid with cash) 200,000 Factory overhead Indirect materials 9,000 Indirect labor 46,000 Other overhead costs 119,000 Sales (received in cash) 1,600,000 Predetermined overhead rate based on direct labor cost 55% No Account Secil 194.000 0 200.000 Foro Use "given" and your "results from HW 2.1 Question 8 on CONNECT relating to Lock-Tite Company to complete the Project requirements below. Make sure you are using CORRECT answers from connect. *No room for summary 1) Write summary journal entries for Lock-Tite Company for the following transactions for the period as calculated/given in the problem on CONNECT. THES Debit Credit a) Purchase of raw material, (To record the purchase of raw materials on a Cash 194,000 b) Transfer of Raw material to Factory 9,000 be (o record that an alternate Work in Proces and Factory Overhead and indirect materials or factory overhea 170,000 c) Recognition of Payroll as indirect and direct labor. 179.ODO Cto record the recognition of peynil os dirt and C. TA 46.000 indirect Labor 154. OD d) Application of Factory Overhead to Work-in-Process (to record over applied overhead) D. 84,700 c) Transfer of Work-in-Process to Finished Goods Del 84,700 "To record the transfer of work in process to finished gold) E. 318.800 Try Werke f) Revenue for the sale of goods manufactured Tentory 1398,800 (To record the cash sales Cash 1,600,000 Solos Ronnie g) Cost of goods sold 1,600,000 G cost of goods 425.000 Fleshed GOODS 425,600 h) The incurrence of the other overhead costs (use "various" to represent multiple accounts) H. (To record the incurrence of other overhead costs) Some Over 114.000 Various 119,000 2) Adjusting Factory Overhead: Include the balance of the COGS account from your connect problem in the T account blow. Indirect Material $9.000 Debit Credit Indirect labor 346,000 COGS Olles overhead Cost of goods Factory sold Overhead Total Achourel Factory booked 174,000 Loss-Aplied factory i Cirkal 194,700 29. 300 (154.0008567 Under-Applied Overhead $89,300 Assume Lock-Tite clears all its under-or over-applied overhead to cost of goods sold. Write the adjusting journal entry to zero the Factory Overhead account. b) Post the journal entry to the COGS T account below and calculate the "adjusted Cost of Goods Sold". The Adjusted Cost of Goods sold Unadjusted Balance $425,600 (to record the cast of goods sold) ests Under Applied Overhead & 89, 300 balance is $514,900. Adjusted Balance 514,900 3) Prepare a Schedule of cost of goods Manufactured using the following: LOCK-TITE COMPANY Schedulo of Cost of Goods Manufactured For Month Ended May 31, Yoar X Direct materials Raw materials inventory, beginning 26,000 Add: Raw materials purchases 1194,000 Raw materials available for use 1220, DDO Less: Raw materials inventory ending 341. DOD Raw materials used 1179 DOD Less: Indirect material used $9.000 Direct Material used 170,000 Direct labor 1154.DDD Factory overhead applied $84,700 Total manufacturing costs 1408.700 Add: Work in process inventory, beginning $9.500 Total cost of work in process :18.200 Less: Work in process inventory, ending $19,400 Cost of Goods Manufactured 398.800 4) Complete the partial income statement for the table below: 31.600.000 Lock-Tite Company Income Statement For Month Ended May 31, Year 1 Sales Cost of goods sold Finished goods inventory, beginning Cost of goods manufactured Cost of goods available for sale Less: Finished goods inventory, ending Unadjusted Cost of goods sold Add/Subtract over/under applied overhead Adjusted Cost of Goods Sold Gross profit $ 61,000 Is 398.800 $ 459,800 34,200 $ 425,600 89.300 $ 514.900 1,085,100 5) Understanding application of Overhead: Many of the terms relating to overhead can become confusing as there are 3 different amounts that need to be considered: BUDGETED (also referred to as estimated) Overhead, APPLIED Overhead and ACTUAL Overhead. Budgcted overhead is established BEFORE an accounting period and is used to establish the predetermined overhead rate. APPLIED overhead is calculated DURING the accounting period as production jobs are completed and costs accumulate in WIP before transferring to FG inventory. ACTUAL overhead is known AFTER or at the end of an accounting period once all costs have been incurred and recorded in the accounting system. The CONNECT problem gives us the APPLIED and ACTUAL amounts of overhead for Lock-Tite Company for the accounting period but not the BUDGETED. Using the 55% predetermined rate, we can infer the BUDGETED overhead for Lock-Tite. Connect indicates that Lock-Tite applies overhead using predetermined overhead rate based on direct labor dollars as their driver. We will look at what would happen if Lock-Tite used a different driver to apply their overhead. Using the following formulas as appropriate below. (*1) Predetermined OH rate = Budgeted/Estimated FOH S Budected drives per driver (2) Applied OH $ = Predetermined OH rate x Actual drivers from JE d) above a) First assume the company budgeted direct labor costs were 1.4 times the actual direct labor. (Amount from le) x 1.4). Include this amount as the "estimated driver amount in the first column (Using DLSs") of the table below. 0.55 = Budgeted/Estimated FOHS (1.ADES b) Use the formula in (*1) and calculate the company's budgeted estimated factory overhead. Include the amount in the table below. This budgeted estimated overhead amount will be used in all three scenarios. You can include this amount in the top row of all three columns c) Complete the first column of the comparison table below. The first column represents what Lock-Tite did use during the month of May. The actual driver amount" should equal the direct labor costs recognized in journal entry from 1c. The applied factory overhead amount should equal the amount recorded in journal entry from ld. The over- or under-applied overhead should equal the amount recorded in journal entry from 2a. Include the words "over" or "under" to indicate if overhead was over- or under-applied during May. Factory Overhead method comparisons Using DL SS Using DL hours Using Machine Hours Budgeted OH in Dollars-calculated in 5b Estimated driver amount 10,000 DL hours 14,000 Machine hours 0.55 7,800 DL hours Predetermined overhead rate Actual driver amounts Applied factory overhead over/under applied factory overhead amount Over or Under-applied? 13,800 hours d) As alternatives, Lock-Tite could use direct labor hours of machine hours to apply overhead. Assume Lock-Tite had originally estimated budgeted 10,000 direct labor hours and 14,000 machine hours, calculate the alternative predetermined rates and include them in the table comparison above. Hint: Use formula (*1) above and remember that budgeted/estimated overhead (first row) will be the same in all three situations. Show 2 decimals 3 e) Assume Lock-Tite's assembly workers worked 7,800 hours during May and production machinery operated for 13,800 hours. Complete the table for the last 2 columns by calculating the amount of overhead they would have applied to Work-In-Process during the month and the amount of over- or under-applied overhead. Use formula (*2). f) Rewrite the journal entry (from 2 above) that would have been required to clear the Factory overhead account assuming the company applied overhead using i) Direct labor hours: ii) Machine hours: g) Think about the relationship of budgeted overhead to the amount of overhead applied. Given that the "drivers" were estimated to be higher than they were, does it make sense that overhead was underapplied? Compare the actual overhead with the estimated/budgeted overhead. What do you think is happening? Explain using 30 to 50 words. h) Would using a different driver significantly affect the amount of Cost of Goods Sold recorded on the income statement for May? Why or why not? Explain using 10 to 30 words. 5) Understanding application of Overhead: Many of the terms relating to overhead can become confusing as there are 3 different amounts that need to be considered; BUDGETED (also referred to as estimated) Overhead, APPLIED Overhead and ACTUAL Overhead. Budgeted overhead is established BEFORE an accounting period and is used to establish the predetermined overhead rate. APPLIED overhead is calculated DURING the accounting period as production jobs are completed and costs accumulate in WIP before transferring to FG inventory. ACTUAL overhead is known AFTER or at the end of an accounting period once all costs have been incurred and recorded in the accounting system. The CONNECT problem gives us the APPLIED and ACTUAL amounts of overhead for Lock-Tite Company for the accounting period but not the BUDGETED. Using the 55% predetermined rate, we can infer the BUDGETED Overhead for Lock-Tite. Connect indicates that Lock-Tite applies overhead using predetermined overhead rate based on direct labor dollars as their driver. We will look at what would happen if Lock-Tite used a different driver to apply their overhead. Using the following formulas as appropriate below. (*1) Predetermined OH rate = Budgeted/Estimated FOH Ss/Budgeted drive-S per driver (2) Applied OH $ - Predetermined OH rate x Actual driver - S from JE d) above a) First assume the company budgeted direct labor costs were 1.4 times the actual direct labor. (Amount from le) x 1.4). Include this amount as the "estimated driver amount" in the first column ("Using DLSs") of the table below. 0.55 - Budgeted/Estimated FOHS/(1-4XDLSS b) Use the formula in (*1) and calculate the company's budgeted/estimated factory overhead. Include the amount in the table below. This budgeted/estimated overhead amount will be used in all three scenarios. You can include this amount in the top row of all three columns. c) Complete the first column of the comparison table below. The first column represents what Lock-Tite did use during the month of May. The "actual driver amount" should equal the direct labor costs recognized in journal entry from 1c. The applied factory overhead amount should equal the amount recorded in journal entry from 1d. The over- or under-applied overhead should equal the amount recorded in journal entry from 2a. Include the words "over" or "under" to indicate if overhead was over- or under-applied during May. Factory Overhead method comparisons Using DL Ss Using DL hours Using Machine Hours Budgeted OH in Dollars - calculated in 5b Estimated driver amount 10,000 14,000 DL hours Machine hours Predetermined overhead rate 0.55 Actual driver amounts 7,800 DL hours 13.800 hours Applied factory overhead over/under) applied factory overhead amount Over or Under-applied? d) As alternatives, Lock-Tite could use direct labor hours or machine hours to apply overhead. Assume Lock-Tite had originally estimated/budgeted 10,000 direct labor hours and 14,000 machine hours, calculate the alternative predetermined rates and include them in the table comparison above. Hint: Use formula (*1) above and remember that budgeted/estimated overhead (first row) will be the same in all three situations. Show 2 decimals e) Assume Lock-Tite's assembly workers worked 7,800 hours during May and production machinery operated for 13,800 hours. Complete the table for the last 2 columns by calculating the amount of overhead they would have applied to Work-In-Process during the month and the amount of over- or under-applied overhead. Use formula (*2). f) Rewrite the journal entry (from 2 above) that would have been required to clear the Factory overhead account assuming the company applied overhead using i) Direct labor hours: ii) Machine hours: g) Think about the relationship of budgeted overhead to the amount of overhead applied. Given that the "drivers were estimated to be higher than they were, does it make sense that overhead was underapplied? Compare the actual overhead with the estimated/budgeted overhead. What do you think is happening? Explain using 30 to 50 words. h) Would using a different driver significantly affect the amount of Cost of Goods Sold recorded on the income statement for May? Why or why not? Explain using 10 to 30 words. Raw Materials (RM) RM - April 30 RM purchases 26,000 194,000 9,000 Indirect materials 170,000 DM used RM-May 31 41.000 Direct Labor Factory payroll 200,000 46,000 indirect labor 154,000 DL used Factory Overhead Indirect materials Indirect labor Other overhead costs 9,000 46,000 119.000 84,700 Overhead applied Underapplied OH 89,300 Work in Process (WIP) GIP - April 30 DM used DL used Overhead applied GIP - May 31 9.500 170,000 154.000 84,700 19,400 398.800 Cost of goods manufactured Finished Goods (FG) FG - April 30 Cost of goods manuf 61.000 398,800 425,600 Cost of goods sold FG - May 31 34,200 Income statement (partial) Sales Cost of goods sold Gross profit 1,600,000 425,600 1,174,400 [The following information applies to the questions displayed below.) The following information is available for Lock-Tite Company, which produces special-order security products and uses a job order costing system. April 30 May 31 Inventories Raw materials $ 26,000 $ 41,000 Work in process 9,500 19,400 Finished goods 61,000 34,200 Activities and Information for May Raw materials purchases (pald with cash) 194,000 Factory payroll (paid with cash) 200,000 Factory overhead Indirect materials 9,000 Indirect labor 46,000 Other overhead costs 119,000 Sales (received in cash) 1,600,000 Predetermined overhead rate based on direct labor cost 55% No Account Secil 194.000 0 200.000 Foro Use "given" and your "results from HW 2.1 Question 8 on CONNECT relating to Lock-Tite Company to complete the Project requirements below. Make sure you are using CORRECT answers from connect. *No room for summary 1) Write summary journal entries for Lock-Tite Company for the following transactions for the period as calculated/given in the problem on CONNECT. THES Debit Credit a) Purchase of raw material, (To record the purchase of raw materials on a Cash 194,000 b) Transfer of Raw material to Factory 9,000 be (o record that an alternate Work in Proces and Factory Overhead and indirect materials or factory overhea 170,000 c) Recognition of Payroll as indirect and direct labor. 179.ODO Cto record the recognition of peynil os dirt and C. TA 46.000 indirect Labor 154. OD d) Application of Factory Overhead to Work-in-Process (to record over applied overhead) D. 84,700 c) Transfer of Work-in-Process to Finished Goods Del 84,700 "To record the transfer of work in process to finished gold) E. 318.800 Try Werke f) Revenue for the sale of goods manufactured Tentory 1398,800 (To record the cash sales Cash 1,600,000 Solos Ronnie g) Cost of goods sold 1,600,000 G cost of goods 425.000 Fleshed GOODS 425,600 h) The incurrence of the other overhead costs (use "various" to represent multiple accounts) H. (To record the incurrence of other overhead costs) Some Over 114.000 Various 119,000 2) Adjusting Factory Overhead: Include the balance of the COGS account from your connect problem in the T account blow. Indirect Material $9.000 Debit Credit Indirect labor 346,000 COGS Olles overhead Cost of goods Factory sold Overhead Total Achourel Factory booked 174,000 Loss-Aplied factory i Cirkal 194,700 29. 300 (154.0008567 Under-Applied Overhead $89,300 Assume Lock-Tite clears all its under-or over-applied overhead to cost of goods sold. Write the adjusting journal entry to zero the Factory Overhead account. b) Post the journal entry to the COGS T account below and calculate the "adjusted Cost of Goods Sold". The Adjusted Cost of Goods sold Unadjusted Balance $425,600 (to record the cast of goods sold) ests Under Applied Overhead & 89, 300 balance is $514,900. Adjusted Balance 514,900 3) Prepare a Schedule of cost of goods Manufactured using the following: LOCK-TITE COMPANY Schedulo of Cost of Goods Manufactured For Month Ended May 31, Yoar X Direct materials Raw materials inventory, beginning 26,000 Add: Raw materials purchases 1194,000 Raw materials available for use 1220, DDO Less: Raw materials inventory ending 341. DOD Raw materials used 1179 DOD Less: Indirect material used $9.000 Direct Material used 170,000 Direct labor 1154.DDD Factory overhead applied $84,700 Total manufacturing costs 1408.700 Add: Work in process inventory, beginning $9.500 Total cost of work in process :18.200 Less: Work in process inventory, ending $19,400 Cost of Goods Manufactured 398.800 4) Complete the partial income statement for the table below: 31.600.000 Lock-Tite Company Income Statement For Month Ended May 31, Year 1 Sales Cost of goods sold Finished goods inventory, beginning Cost of goods manufactured Cost of goods available for sale Less: Finished goods inventory, ending Unadjusted Cost of goods sold Add/Subtract over/under applied overhead Adjusted Cost of Goods Sold Gross profit $ 61,000 Is 398.800 $ 459,800 34,200 $ 425,600 89.300 $ 514.900 1,085,100 5) Understanding application of Overhead: Many of the terms relating to overhead can become confusing as there are 3 different amounts that need to be considered: BUDGETED (also referred to as estimated) Overhead, APPLIED Overhead and ACTUAL Overhead. Budgcted overhead is established BEFORE an accounting period and is used to establish the predetermined overhead rate. APPLIED overhead is calculated DURING the accounting period as production jobs are completed and costs accumulate in WIP before transferring to FG inventory. ACTUAL overhead is known AFTER or at the end of an accounting period once all costs have been incurred and recorded in the accounting system. The CONNECT problem gives us the APPLIED and ACTUAL amounts of overhead for Lock-Tite Company for the accounting period but not the BUDGETED. Using the 55% predetermined rate, we can infer the BUDGETED overhead for Lock-Tite. Connect indicates that Lock-Tite applies overhead using predetermined overhead rate based on direct labor dollars as their driver. We will look at what would happen if Lock-Tite used a different driver to apply their overhead. Using the following formulas as appropriate below. (*1) Predetermined OH rate = Budgeted/Estimated FOH S Budected drives per driver (2) Applied OH $ = Predetermined OH rate x Actual drivers from JE d) above a) First assume the company budgeted direct labor costs were 1.4 times the actual direct labor. (Amount from le) x 1.4). Include this amount as the "estimated driver amount in the first column (Using DLSs") of the table below. 0.55 = Budgeted/Estimated FOHS (1.ADES b) Use the formula in (*1) and calculate the company's budgeted estimated factory overhead. Include the amount in the table below. This budgeted estimated overhead amount will be used in all three scenarios. You can include this amount in the top row of all three columns c) Complete the first column of the comparison table below. The first column represents what Lock-Tite did use during the month of May. The actual driver amount" should equal the direct labor costs recognized in journal entry from 1c. The applied factory overhead amount should equal the amount recorded in journal entry from ld. The over- or under-applied overhead should equal the amount recorded in journal entry from 2a. Include the words "over" or "under" to indicate if overhead was over- or under-applied during May. Factory Overhead method comparisons Using DL SS Using DL hours Using Machine Hours Budgeted OH in Dollars-calculated in 5b Estimated driver amount 10,000 DL hours 14,000 Machine hours 0.55 7,800 DL hours Predetermined overhead rate Actual driver amounts Applied factory overhead over/under applied factory overhead amount Over or Under-applied? 13,800 hours d) As alternatives, Lock-Tite could use direct labor hours of machine hours to apply overhead. Assume Lock-Tite had originally estimated budgeted 10,000 direct labor hours and 14,000 machine hours, calculate the alternative predetermined rates and include them in the table comparison above. Hint: Use formula (*1) above and remember that budgeted/estimated overhead (first row) will be the same in all three situations. Show 2 decimals 3 e) Assume Lock-Tite's assembly workers worked 7,800 hours during May and production machinery operated for 13,800 hours. Complete the table for the last 2 columns by calculating the amount of overhead they would have applied to Work-In-Process during the month and the amount of over- or under-applied overhead. Use formula (*2). f) Rewrite the journal entry (from 2 above) that would have been required to clear the Factory overhead account assuming the company applied overhead using i) Direct labor hours: ii) Machine hours: g) Think about the relationship of budgeted overhead to the amount of overhead applied. Given that the "drivers" were estimated to be higher than they were, does it make sense that overhead was underapplied? Compare the actual overhead with the estimated/budgeted overhead. What do you think is happening? Explain using 30 to 50 words. h) Would using a different driver significantly affect the amount of Cost of Goods Sold recorded on the income statement for May? Why or why not? Explain using 10 to 30 words. 5) Understanding application of Overhead: Many of the terms relating to overhead can become confusing as there are 3 different amounts that need to be considered; BUDGETED (also referred to as estimated) Overhead, APPLIED Overhead and ACTUAL Overhead. Budgeted overhead is established BEFORE an accounting period and is used to establish the predetermined overhead rate. APPLIED overhead is calculated DURING the accounting period as production jobs are completed and costs accumulate in WIP before transferring to FG inventory. ACTUAL overhead is known AFTER or at the end of an accounting period once all costs have been incurred and recorded in the accounting system. The CONNECT problem gives us the APPLIED and ACTUAL amounts of overhead for Lock-Tite Company for the accounting period but not the BUDGETED. Using the 55% predetermined rate, we can infer the BUDGETED Overhead for Lock-Tite. Connect indicates that Lock-Tite applies overhead using predetermined overhead rate based on direct labor dollars as their driver. We will look at what would happen if Lock-Tite used a different driver to apply their overhead. Using the following formulas as appropriate below. (*1) Predetermined OH rate = Budgeted/Estimated FOH Ss/Budgeted drive-S per driver (2) Applied OH $ - Predetermined OH rate x Actual driver - S from JE d) above a) First assume the company budgeted direct labor costs were 1.4 times the actual direct labor. (Amount from le) x 1.4). Include this amount as the "estimated driver amount" in the first column ("Using DLSs") of the table below. 0.55 - Budgeted/Estimated FOHS/(1-4XDLSS b) Use the formula in (*1) and calculate the company's budgeted/estimated factory overhead. Include the amount in the table below. This budgeted/estimated overhead amount will be used in all three scenarios. You can include this amount in the top row of all three columns. c) Complete the first column of the comparison table below. The first column represents what Lock-Tite did use during the month of May. The "actual driver amount" should equal the direct labor costs recognized in journal entry from 1c. The applied factory overhead amount should equal the amount recorded in journal entry from 1d. The over- or under-applied overhead should equal the amount recorded in journal entry from 2a. Include the words "over" or "under" to indicate if overhead was over- or under-applied during May. Factory Overhead method comparisons Using DL Ss Using DL hours Using Machine Hours Budgeted OH in Dollars - calculated in 5b Estimated driver amount 10,000 14,000 DL hours Machine hours Predetermined overhead rate 0.55 Actual driver amounts 7,800 DL hours 13.800 hours Applied factory overhead over/under) applied factory overhead amount Over or Under-applied? d) As alternatives, Lock-Tite could use direct labor hours or machine hours to apply overhead. Assume Lock-Tite had originally estimated/budgeted 10,000 direct labor hours and 14,000 machine hours, calculate the alternative predetermined rates and include them in the table comparison above. Hint: Use formula (*1) above and remember that budgeted/estimated overhead (first row) will be the same in all three situations. Show 2 decimals e) Assume Lock-Tite's assembly workers worked 7,800 hours during May and production machinery operated for 13,800 hours. Complete the table for the last 2 columns by calculating the amount of overhead they would have applied to Work-In-Process during the month and the amount of over- or under-applied overhead. Use formula (*2). f) Rewrite the journal entry (from 2 above) that would have been required to clear the Factory overhead account assuming the company applied overhead using i) Direct labor hours: ii) Machine hours: g) Think about the relationship of budgeted overhead to the amount of overhead applied. Given that the "drivers were estimated to be higher than they were, does it make sense that overhead was underapplied? Compare the actual overhead with the estimated/budgeted overhead. What do you think is happening? Explain using 30 to 50 words. h) Would using a different driver significantly affect the amount of Cost of Goods Sold recorded on the income statement for May? Why or why not? Explain using 10 to 30 words

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts