Question: Question 6 ( 4 points ) Consider the following returns: table [ [ Year - End,Home Depot Realized Return,IBM Realized Return ] , [

Question points

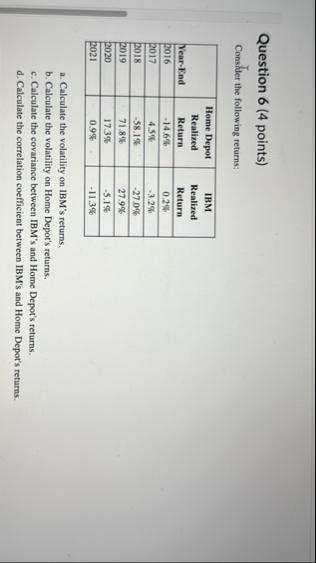

Consider the following returns:

tableYearEnd,Home Depot Realized Return,IBM Realized Return

a Calculate the volatility on IBM's returns.

b Calculate the volatility on Home Depot's returns.

c Calculate the covariance between IBM's and Home Depot's returns.

d Calculate the correlation coefficient between IBM's and Home Depot's returns.

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock