Question: question 6 Q6 Consider the following information regarding the performance of a money manager in recent month. The table represents the actual return of each

question 6

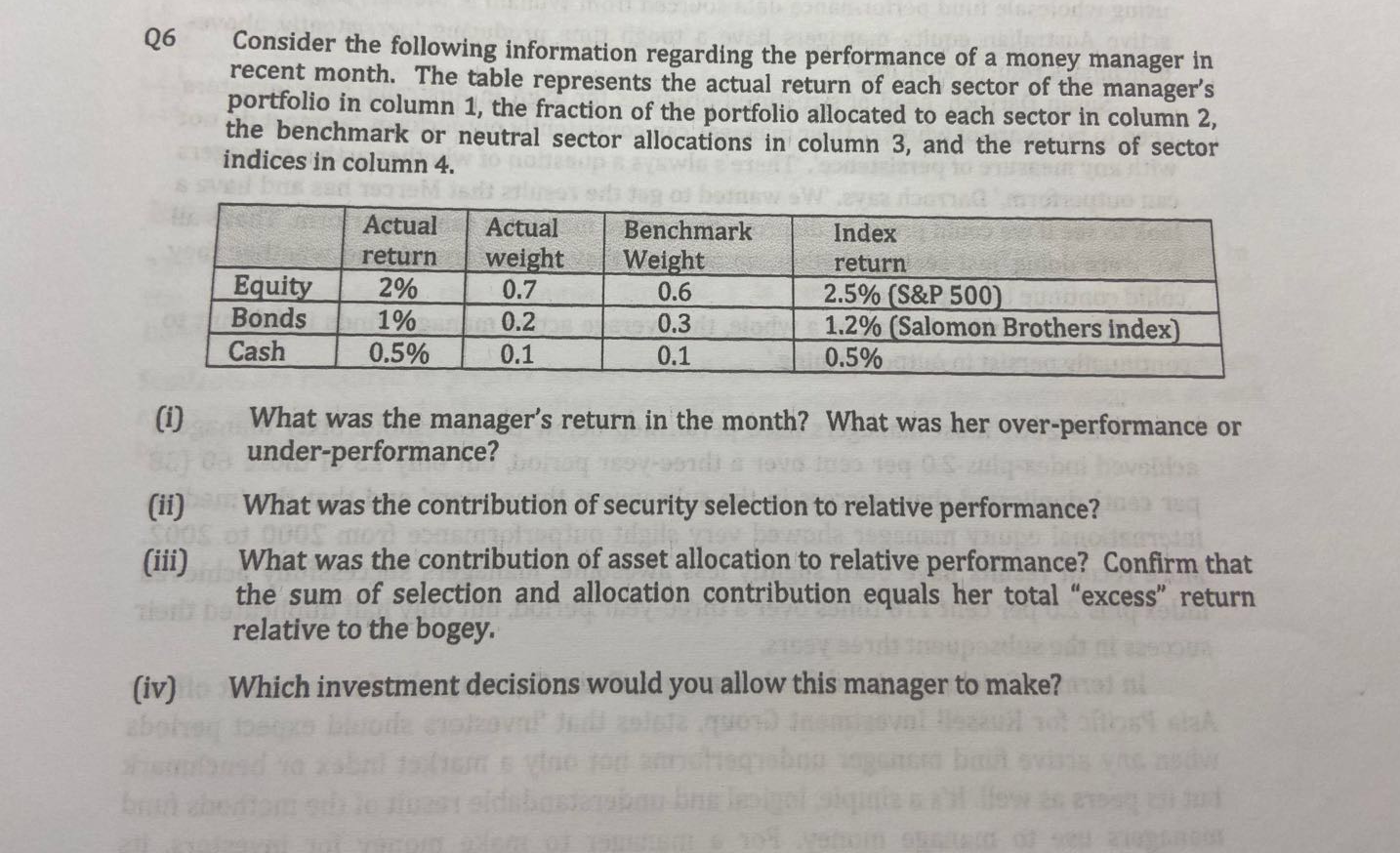

Q6 Consider the following information regarding the performance of a money manager in recent month. The table represents the actual return of each sector of the manager's portfolio in column 1, the fraction of the portfolio allocated to each sector in column 2, the benchmark or neutral sector allocations in column 3, and the returns of sector indices in column 4. Equity Bonds Cash Actual return 2% 1% 0.5% Actual weight 0.7 0.2 0.1 Benchmark Weight 0.6 0.3 0.1 Index return 2.5% (S&P 500) 1.2% (Salomon Brothers index 0.5% What was the manager's return in the month? What was her over-performance or under-performance? (ii) What was the contribution of security selection to relative performance? What was the contribution of asset allocation to relative performance? Confirm that the sum of selection and allocation contribution equals her total "excess" return relative to the bogey. (iv) Which investment decisions would you allow this manager to make

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts