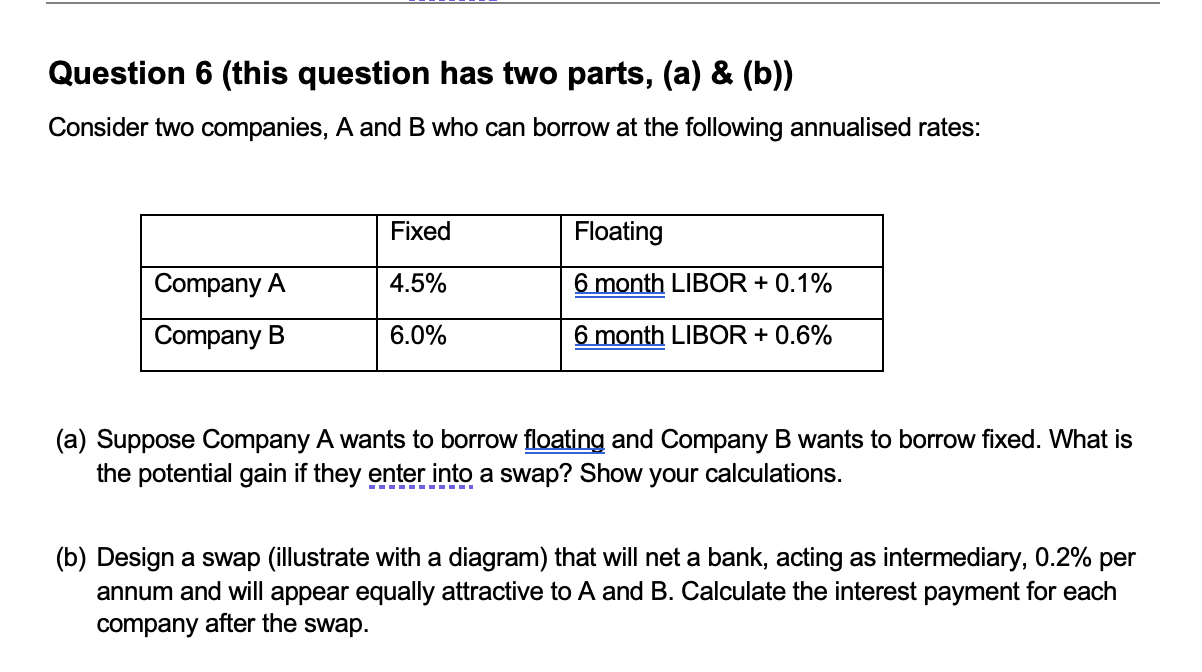

Question: Question 6 (this question has two parts, (a) & (b)) Consider two companies, A and B who can borrow at the following annualised rates: Fixed

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock