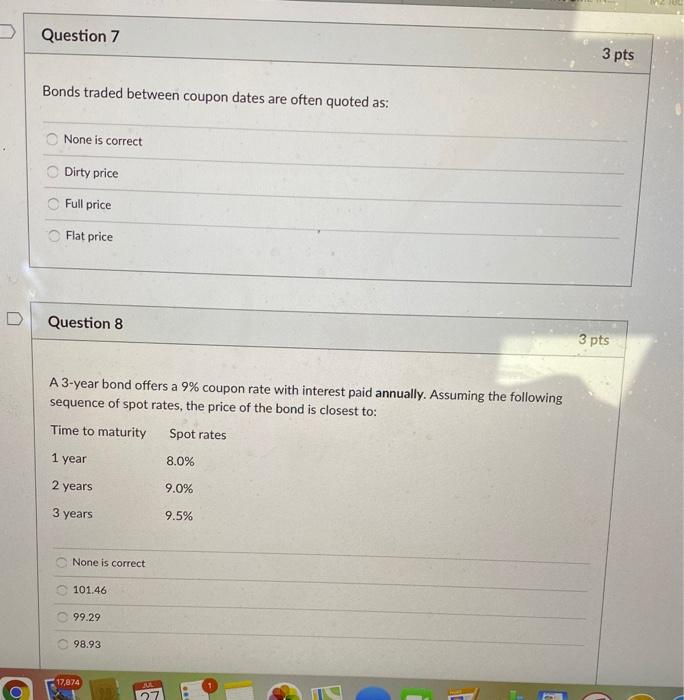

Question: Question 7 3 pts Bonds traded between coupon dates are often quoted as: None is correct Dirty price Full price Flat price D Question 8

Question 7 3 pts Bonds traded between coupon dates are often quoted as: None is correct Dirty price Full price Flat price D Question 8 3 pts A 3-year bond offers a 9% coupon rate with interest paid annually. Assuming the following sequence of spot rates, the price of the bond is closest to: Time to maturity Spot rates 1 year 8.0% 2 years 9.0% 3 years 9.5% None is correct 101.46 99.29 98.93 17,074

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock