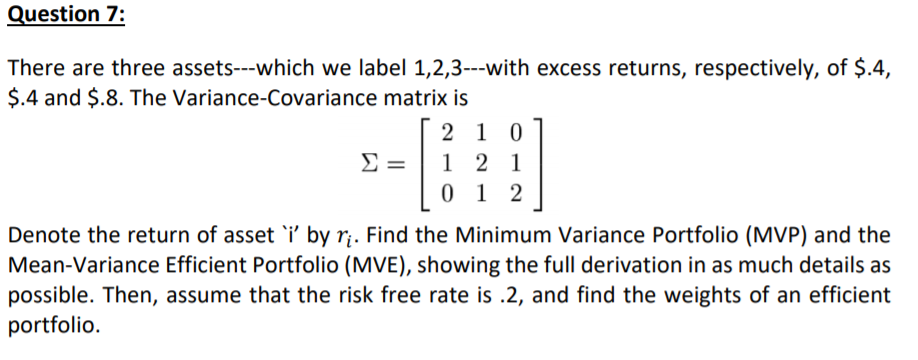

Question: Question 7: There are three assets---which we label 1,2,3---with excess returns, respectively, of $.4, $.4 and $.8. The Variance-Covariance matrix is 2 1 0 =

Question 7: There are three assets---which we label 1,2,3---with excess returns, respectively, of $.4, $.4 and $.8. The Variance-Covariance matrix is 2 1 0 = 1 2 1 0 1 2 Denote the return of asset by ri. Find the Minimum Variance Portfolio (MVP) and the Mean-Variance Efficient Portfolio (MVE), showing the full derivation in as much details as possible. Then, assume that the risk free rate is .2, and find the weights of an efficient portfolio

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock