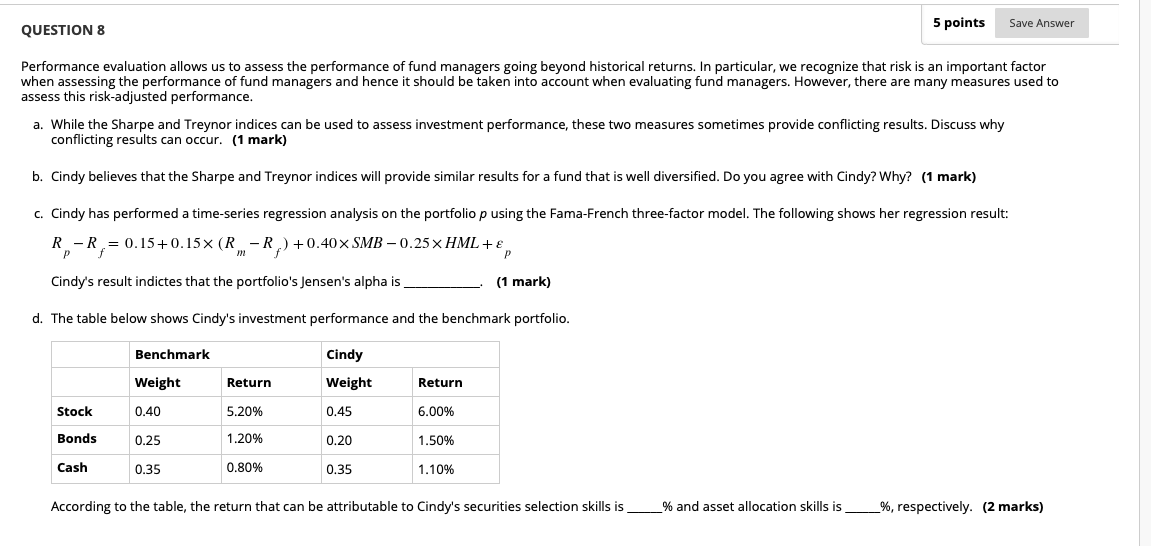

Question: QUESTION 8 5 points Save Answer Performance evaluation allows us to assess the performance of fund managers going beyond historical returns. In particular, we recognize

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts