Question: Question 8 6 pts Consider two bonds, both pay annual interest. Bond has a coupon of per year, maturity of years, yield to maturity of

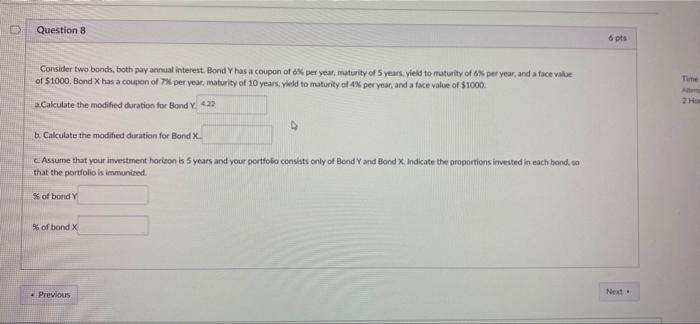

Question 8 6 pts Consider two bonds, both pay annual interest. Bond has a coupon of per year, maturity of years, yield to maturity of per year and a face value of $1000 Bond X has a coupon of 7% per year, maturity of 10 years, yield to maturity of 4% per year, and a face value of $1000 Time 2 Ho Calculate the modified duration for Bond Y. 422 b. Calculate the modified duration for Bond X C. Assume that your investment horison is 5 years and your portfolio consists only of Bond Y and Bond X Indicate the proportions invested in each bond, 10 that the portfolio is immunited. of bond Y % of bond X Previous Ned

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock