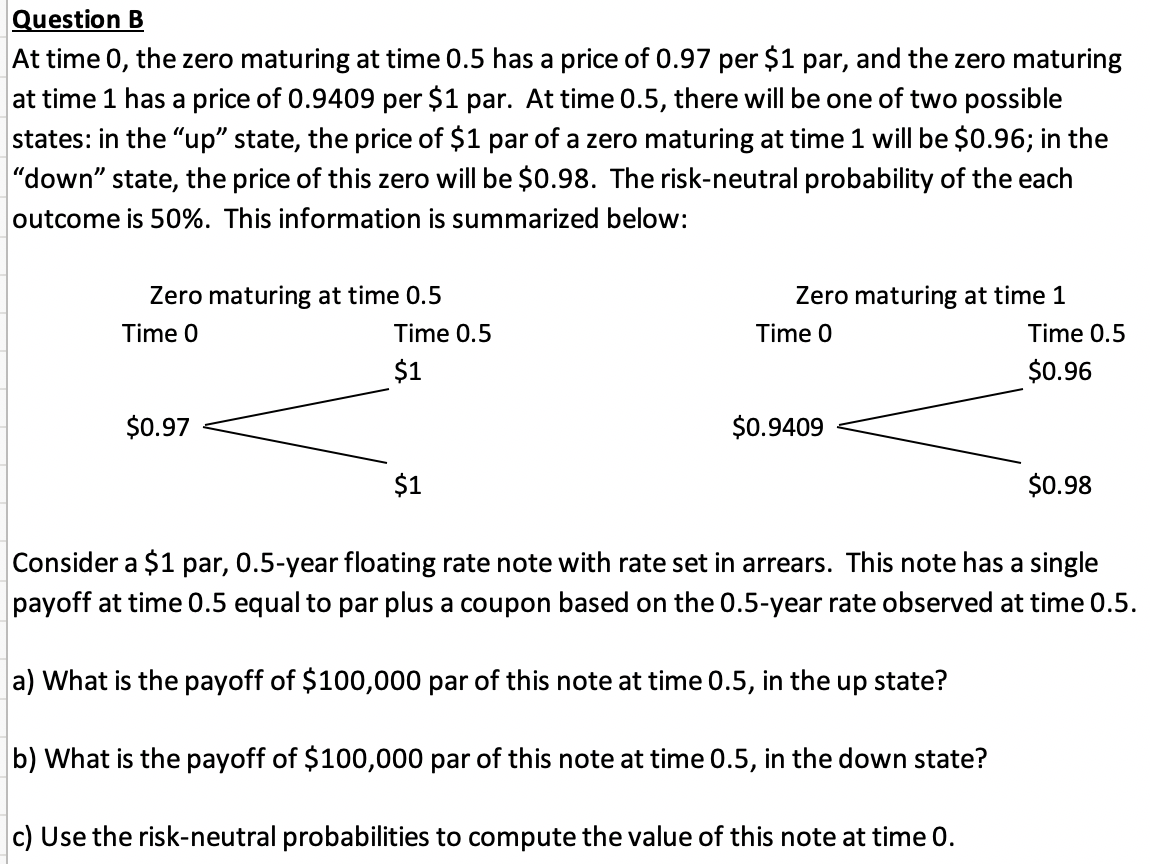

Question: Question B At time 0, the zero maturing at time 0.5 has a price of 0.97 per $1 par, and the zero maturing at

Question B At time 0, the zero maturing at time 0.5 has a price of 0.97 per $1 par, and the zero maturing at time 1 has a price of 0.9409 per $1 par. At time 0.5, there will be one of two possible states: in the "up" state, the price of $1 par of a zero maturing at time 1 will be $0.96; in the "down" state, the price of this zero will be $0.98. The risk-neutral probability of the each outcome is 50%. This information is summarized below: Zero maturing at time 0.5 Time 0 Time 0.5 $1 Zero maturing at time 1 Time 0 Time 0.5 $0.96 $0.97 $1 $0.9409 $0.98 Consider a $1 par, 0.5-year floating rate note with rate set in arrears. This note has a single payoff at time 0.5 equal to par plus a coupon based on the 0.5-year rate observed at time 0.5. a) What is the payoff of $100,000 par of this note at time 0.5, in the up state? b) What is the payoff of $100,000 par of this note at time 0.5, in the down state? c) Use the risk-neutral probabilities to compute the value of this note at time 0.

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts