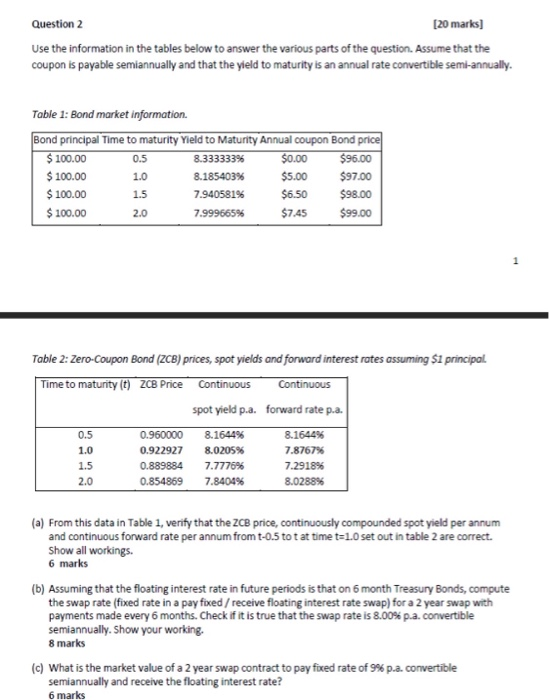

Question: question b Question 2 [20 marks) Use the information in the tables below to answer the various parts of the question. Assume that the coupon

Question 2 [20 marks) Use the information in the tables below to answer the various parts of the question. Assume that the coupon is payable semiannually and that the yield to maturity is an annual rate convertible semi-annually. Table 1: Bond market information. Bond principal Time to maturity Yield to Maturity Annual coupon Bond price $ 100.00 0.5 8.333333% $0.00 $96.00 $ 100.00 1.0 8.185403% $5.00 $97.00 $ 100.00 1.5 7.940581% $6.50 $98.00 $ 100.00 2.0 7.999665% $7.45 $99.00 1 Table 2: Zero-Coupon Bond (2CB) prices, spot yields and forward interest rates assuming $1 principal Time to maturity (t) ZCB Price Continuous Continuous spot yield p.a. forward rate p.a. 0.960000 8.1644% 8.1644% 7.8767% 7.2918% 8.0288% 0.5 1.0 1.5 2.0 0.922927 0.889884 0.854869 8.0205% 7.7776% 7.8404% (a) From this data in Table 1, verify that the ZCB price, continuously compounded spot yield per annum and continuous forward rate per annum from t-o.5 tot at time t=1.0 set out in table 2 are correct. Show all workings. 6 marks (b) Assuming that the floating interest rate in future periods is that on 6 month Treasury Bonds, compute the swap rate (fixed rate in a pay fixed / receive floating interest rate swap) for a 2 year swap with payments made every 6 months. Check if it is true that the swap rate is 8.00% p.a. convertible semiannually. Show your working. 8 marks (c) What is the market value of a 2 year swap contract to pay fixed rate of 9% p.a. convertible semiannually and receive the floating interest rate? 6 marks Question 2 [20 marks) Use the information in the tables below to answer the various parts of the question. Assume that the coupon is payable semiannually and that the yield to maturity is an annual rate convertible semi-annually. Table 1: Bond market information. Bond principal Time to maturity Yield to Maturity Annual coupon Bond price $ 100.00 0.5 8.333333% $0.00 $96.00 $ 100.00 1.0 8.185403% $5.00 $97.00 $ 100.00 1.5 7.940581% $6.50 $98.00 $ 100.00 2.0 7.999665% $7.45 $99.00 1 Table 2: Zero-Coupon Bond (2CB) prices, spot yields and forward interest rates assuming $1 principal Time to maturity (t) ZCB Price Continuous Continuous spot yield p.a. forward rate p.a. 0.960000 8.1644% 8.1644% 7.8767% 7.2918% 8.0288% 0.5 1.0 1.5 2.0 0.922927 0.889884 0.854869 8.0205% 7.7776% 7.8404% (a) From this data in Table 1, verify that the ZCB price, continuously compounded spot yield per annum and continuous forward rate per annum from t-o.5 tot at time t=1.0 set out in table 2 are correct. Show all workings. 6 marks (b) Assuming that the floating interest rate in future periods is that on 6 month Treasury Bonds, compute the swap rate (fixed rate in a pay fixed / receive floating interest rate swap) for a 2 year swap with payments made every 6 months. Check if it is true that the swap rate is 8.00% p.a. convertible semiannually. Show your working. 8 marks (c) What is the market value of a 2 year swap contract to pay fixed rate of 9% p.a. convertible semiannually and receive the floating interest rate? 6 marks

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts