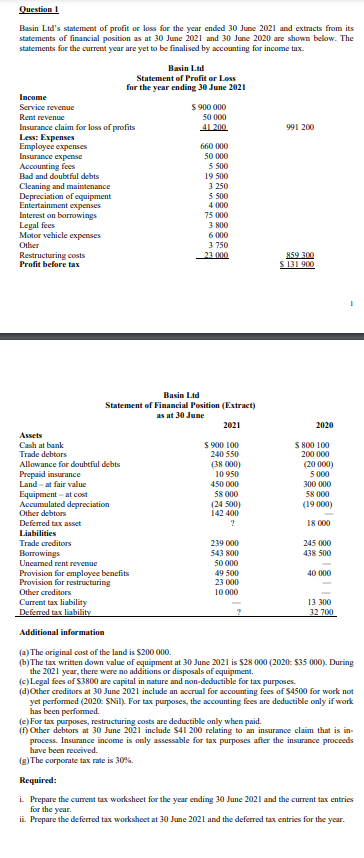

Question! Basin Ltd's statement of profit or loss for the year ended 30 June 2021 and...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

Question! Basin Ltd's statement of profit or loss for the year ended 30 June 2021 and extracts from its statements of financial position as at 30 June 2021 and 30 June 2020 are shown below. The statements for the current year are yet to be finalised by accounting for income tax. Basin Ltd Statement of Profit or Loss for the year ending 30 June 2021 $900 000 Income Service revenue Rent revenue Insurance claim for loss of profits Less: Expenses Employee expenses Insurance expense Accounting fees 50 000 41 200 991 200 660 000 Bad and doubtful debts Cleaning and maintenance Depreciation of equipment Entertainment expenses Interest on borrowings Legal fees Motor vehicle expenses Other Restructuring costs Profit before tax 50 000 5500 19 500 3 250 5 500 4 000 75 000 3 800 6 000 3 750 23 000 859 300 $ 131 900 Basin Ltd Statement of Financial Position (Extract) as at 30 June Assets Cash at bank Trade debtors Allowance for doubtful debts Prepaid insurance Land - at fair value Equipment - at cost Accumulated depreciation Other debtors Deferred tax asset Liabilities Trade creditors Borrowings Unearned rent revenue Provision for employee benefits Provision for restructuring Other creditors Current tax liability Deferred tax liability Additional information 2021 2020 $ 900 100 $ 800 100 240 550 (38 000) 10 950 450 000 58 000 (24 500) 142 400 200 000 (20 000) 5000 300 000 58 000 (19 000) ? 18 000 239 000 245 000 543 800 438 500 50 000 49 500 40 000 23 000 10 000 13 300 32 700 (a) The original cost of the land is $200 000. (b) The tax written down value of equipment at 30 June 2021 is $28 000 (2020: $35 000). During the 2021 year, there were no additions or disposals of equipment. (c) Legal fees of $3800 are capital in nature and non-deductible for tax purposes. (d)Other creditors at 30 June 2021 include an accrual for accounting fees of $4500 for work not yet performed (2020: $Nil). For tax purposes, the accounting fees are deductible only if work has been performed. (e) For tax purposes, restructuring costs are deductible only when paid. (f) Other debtors at 30 June 2021 include $41 200 relating to an insurance claim that is in- process. Insurance income is only assessable for tax purposes after the insurance proceeds have been received. (g) The corporate tax rate is 30%. Required: i. Prepare the current tax worksheet for the year ending 30 June 2021 and the current tax entries for the year. ii. Prepare the deferred tax worksheet at 30 June 2021 and the deferred tax entries for the year. Question! Basin Ltd's statement of profit or loss for the year ended 30 June 2021 and extracts from its statements of financial position as at 30 June 2021 and 30 June 2020 are shown below. The statements for the current year are yet to be finalised by accounting for income tax. Basin Ltd Statement of Profit or Loss for the year ending 30 June 2021 $900 000 Income Service revenue Rent revenue Insurance claim for loss of profits Less: Expenses Employee expenses Insurance expense Accounting fees 50 000 41 200 991 200 660 000 Bad and doubtful debts Cleaning and maintenance Depreciation of equipment Entertainment expenses Interest on borrowings Legal fees Motor vehicle expenses Other Restructuring costs Profit before tax 50 000 5500 19 500 3 250 5 500 4 000 75 000 3 800 6 000 3 750 23 000 859 300 $ 131 900 Basin Ltd Statement of Financial Position (Extract) as at 30 June Assets Cash at bank Trade debtors Allowance for doubtful debts Prepaid insurance Land - at fair value Equipment - at cost Accumulated depreciation Other debtors Deferred tax asset Liabilities Trade creditors Borrowings Unearned rent revenue Provision for employee benefits Provision for restructuring Other creditors Current tax liability Deferred tax liability Additional information 2021 2020 $ 900 100 $ 800 100 240 550 (38 000) 10 950 450 000 58 000 (24 500) 142 400 200 000 (20 000) 5000 300 000 58 000 (19 000) ? 18 000 239 000 245 000 543 800 438 500 50 000 49 500 40 000 23 000 10 000 13 300 32 700 (a) The original cost of the land is $200 000. (b) The tax written down value of equipment at 30 June 2021 is $28 000 (2020: $35 000). During the 2021 year, there were no additions or disposals of equipment. (c) Legal fees of $3800 are capital in nature and non-deductible for tax purposes. (d)Other creditors at 30 June 2021 include an accrual for accounting fees of $4500 for work not yet performed (2020: $Nil). For tax purposes, the accounting fees are deductible only if work has been performed. (e) For tax purposes, restructuring costs are deductible only when paid. (f) Other debtors at 30 June 2021 include $41 200 relating to an insurance claim that is in- process. Insurance income is only assessable for tax purposes after the insurance proceeds have been received. (g) The corporate tax rate is 30%. Required: i. Prepare the current tax worksheet for the year ending 30 June 2021 and the current tax entries for the year. ii. Prepare the deferred tax worksheet at 30 June 2021 and the deferred tax entries for the year.

Expert Answer:

Posted Date:

Students also viewed these finance questions

-

Jogger 1 is travelling east at 6 . 5 m / s and has a mass of 8 2 kg . Jogger 2 is travelling north at 5 . 8 m / s and has a mass of 5 4 . 5 kg . One of the joggers has their head down and doesnt see...

-

Developing an IT Disaster Recovery Plan, After watching the video you are required to create thread discussing at least three concepts presented in or that you learned from the video. Below is the...

-

Rationalize each denominator. Assume that all variables represent positive real numbers and that no denominators are 0. 4 x-2Vy

-

Consider a risk-neutral government-subsidized bank that has an average cost of lending each small loan of $100 to the poor as a function of time where t is the year. The maximum interest rate that...

-

For warranty purposes, analysts want to model the number of defects on a screen of the new tablet they are manufacturing. Let X = the number of defective pixels per screen. If X can be modeled by: a)...

-

1. For each day that Sasha travels to work, the probability that she will experience a delay due to traffic is 0.2. Each day can be considered independent of the other days. (a) For the next 21 days...

-

A GRAY CAST IRON GEAR IS ATTACHED TO A STEEL SHAFT VIA AN INTERFERENCE FIT. USE MODIFIED MOHR (MM) OR BRITTLE COULOMB - MOHR (BCM) TO CALCULATE THE SAFETY FACTOR FOR THE GEAR paa - SUT = 40000 8 INT...

-

Discuss the applicability of the internal control structure components to financing cycle transactions.

-

What are some of the dangers'that face internal auditors if they d^lay their involvement with the computer?

-

Cross-referencing for working papers should be: a. Done after completing the field work. b. Used to confirm data previously recorded. c. Consistently applied. d. Referred to in the audit report. e. a...

-

Describe the nature of each of the following substantive tests and indicate the assertions to which each relates: a. Vouch entries to long-term debt accounts. b. Confirm debt. c. Recalculate interest...

-

Working papers should be so maintained and referenced that they: a. Represent a good historical document. b. Can be readily filed and retrieved. c. Can be readily completed by another auditor if the...

-

Write a program to compute the following Result= (x + y)5 y y 2* Z

-

Find the market equilibrium point for the following demand and supply functions. Demand: 2p = - q + 56 Supply: 3p - q = 34

-

Why are negative coefficients unusual?

-

There are some sceptics who claim that financial analysis serves no purpose. Why? State your views.

-

What other concept does the capital market line bring to mind?

Study smarter with the SolutionInn App