Question: Question Completion Status: 2 26 3 27 8 9 4 28 10 5 29 11 6 30 12 25 13 14 15 16 17 18

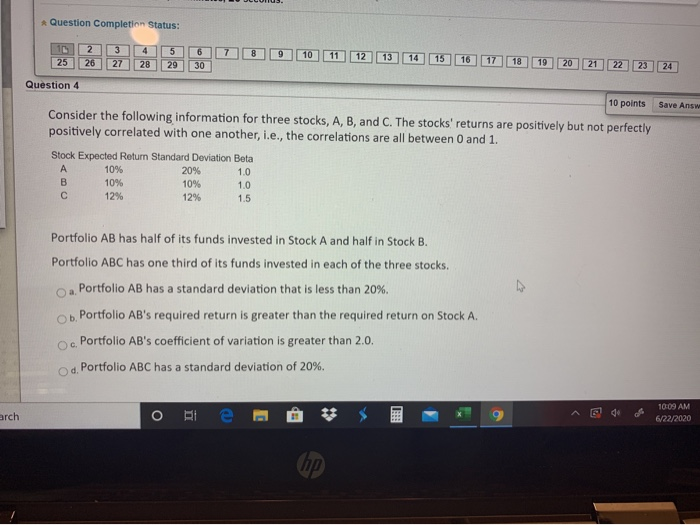

Question Completion Status: 2 26 3 27 8 9 4 28 10 5 29 11 6 30 12 25 13 14 15 16 17 18 19 20 21 22 23 24 Save Answ Question 4 10 points Consider the following information for three stocks, A, B, and C. The stocks' returns are positively but not perfectly positively correlated with one another, i.e., the correlations are all between 0 and 1. Stock Expected Return Standard Deviation Beta 10% 20% B 10% 10% 1.0 12% 1.5 1.0 12% Portfolio AB has half of its funds invested in Stock A and half in Stock B. Portfolio ABC has one third of its funds invested in each of the three stocks, O a Portfolio AB has a standard deviation that is less than 20%. Ob. Portfolio AB's required return is greater than the required return on Stock A. Portfolio AB's coefficient of variation is greater than 2.0. od Portfolio ABC has a standard deviation of 20%. Oo * O # 10:09 AM 6/22/2020 arch )

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts