Question: Question Consider two Assets with the following mean 1=0.10; Variance1 =0.60 mean 2 =0.05; variance2 = 0 Calculate the weights of the portfolio, (w1, w2)

Question Consider two Assets with the following mean 1=0.10; Variance1 =0.60 mean 2 =0.05; variance2 = 0 Calculate the weights of the portfolio, (w1, w2) such that the expected return, Mean weight = 18. Calculate the variance of this portfolio.

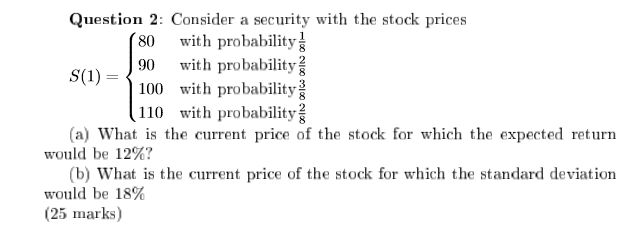

Question 2

Question 2: Consider a security with the stock prices 80 with probability 90 with probability S(1) = 100 with probability (110 with probability (a) What is the current price of the stock for which the expected return would be 12%? (b) What is the current price of the stock for which the standard deviation would be 18% (25 marks) Question 2: Consider a security with the stock prices 80 with probability 90 with probability S(1) = 100 with probability (110 with probability (a) What is the current price of the stock for which the expected return would be 12%? (b) What is the current price of the stock for which the standard deviation would be 18% (25 marks)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts