Question: Question I (a) Explain why the expected utility theory is better than the utility maximization theory that assumes away uncertainty. Your answer must also include

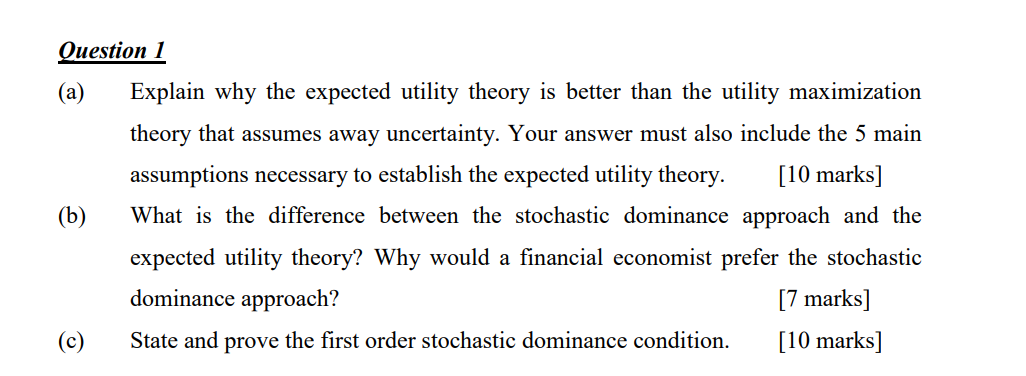

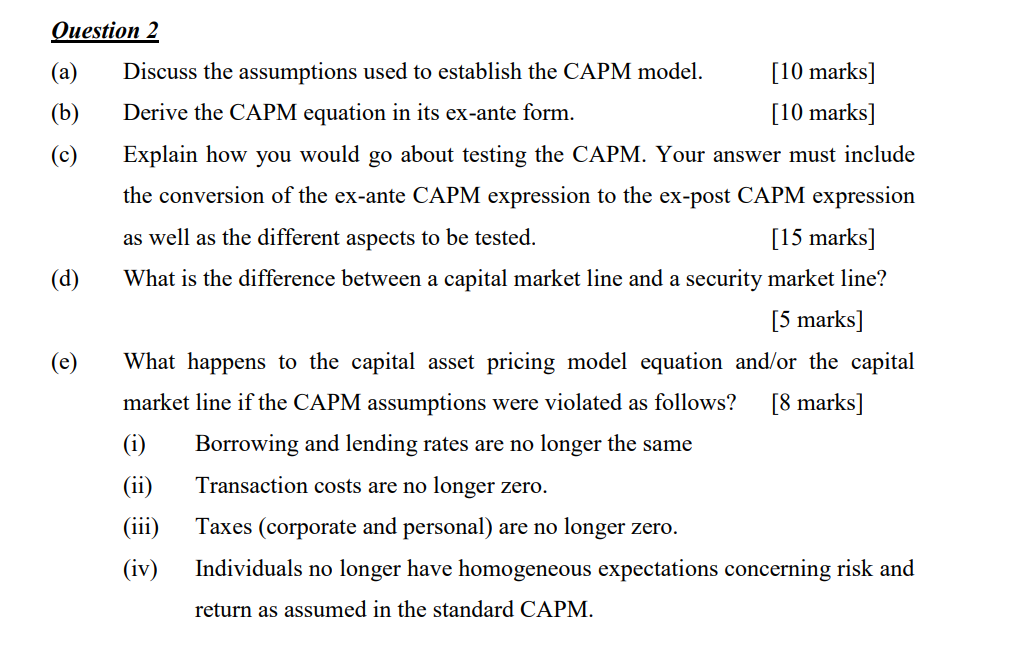

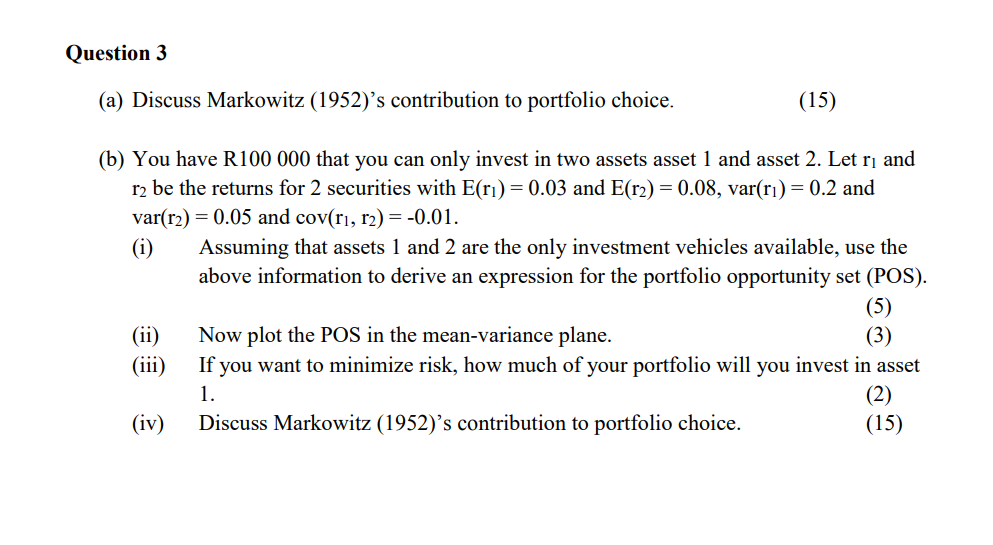

Question I (a) Explain why the expected utility theory is better than the utility maximization theory that assumes away uncertainty. Your answer must also include the 5 main assumptions necessary to establish the expected utility theory. [10 marks] (b) What is the difference between the stochastic dominance approach and the expected utility theory? Why would a nancial economist prefer the stochastic dominance approach? [7 marks] (c) State and prove the first order stochastic dominance condition. [10 marks] Question 2 (a) (b) (C) (d) {6) Discuss the assumptions used to establish the CAPM model. [10 marks] Derive the CAPM equation in its ex-ante form. [10 marks] Explain how you would go about testing the CAPM. Your answer must include the conversion of the ex-ante CAPM expression to the ex-post CAPM expression as well as the different aspects to be tested. [15 marks] What is the difference between a capital market line and a security market line? [5 marks] What happens to the capital asset pricing model equation and/or the capital market line if the CAPM assumptions were violated as follows? [8 marks] (i) Borrowing and lending rates are no longer the same (ii) Transaction costs are no longer zero. (iii) Taxes (corporate and personal) are no longer zero. (iv) Individuals no longer have homogeneous expectations concerning risk and return as assumed in the standard CAPM. Question 3 (a) Discuss Markowitz (1952)'s contribution to portfolio choice. (15) (b) You have R100 000 that you can only invest in two assets asset 1 and asset 2. Let r] and r;- be the returns for 2 securities with E(r1) = 0.03 and E(r2) = 0.08, var(r1) = 0.2 and var(r2) = 0.05 and cov{r1, r2) = -0.01. (i) Assuming that assets 1 and 2 are the only investment vehicles available, use the above information to derive an expression for the portfolio opportunity set (P03). (5) (ii) Now plot the P08 in the mean-variance plane. (3) (iii) If you want to minimize risk, how much of your portfolio will you invest in asset 1. (2) (iv) Discuss Markowitz {1952)'s contribution to portfolio choice. (15)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts